Automated Fare Collection Systems

Automated Fare Collection SystemsAutomated Fare Collection Systems Analysis Report 2025: Market to Grow by a CAGR of XX to 2033, Driven by Government Incentives, Popularity of Virtual Assistants, and Strategic Partnerships

Automated Fare Collection Systems by Type (Near-Field Communication, Magnetic Stripes, OCR, Smart Card, Other), by Application (Transport & Logistic, Media & Entertainment, Government, Retail, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

Automated Fare Collection Systems Analysis Report 2025: Market to Grow by a CAGR of XX to 2033, Driven by Government Incentives, Popularity of Virtual Assistants, and Strategic Partnerships

Automated Fare Collection Systems Analysis Report 2025: Market to Grow by a CAGR of XX to 2033, Driven by Government Incentives, Popularity of Virtual Assistants, and Strategic Partnerships

Key Insights

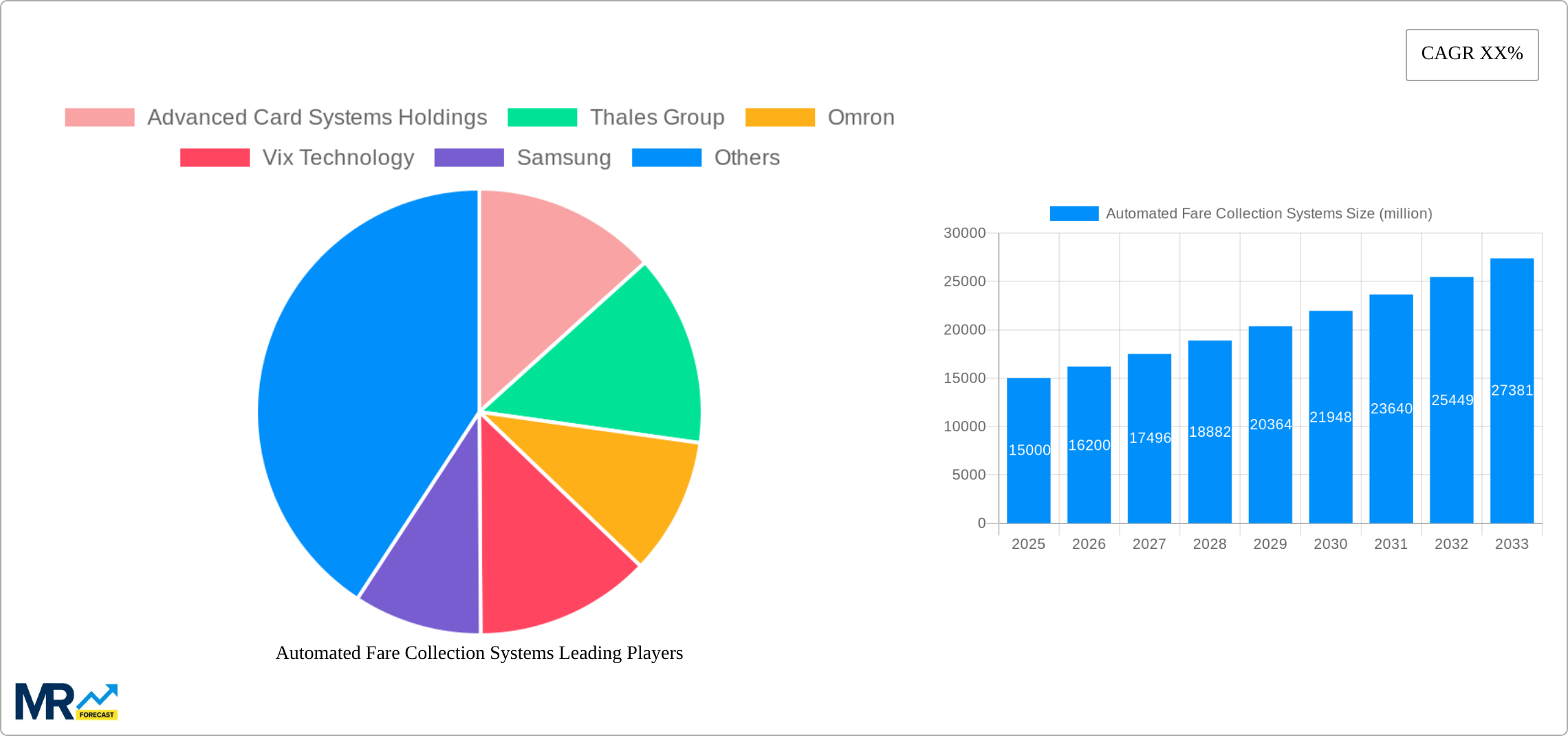

The Automated Fare Collection (AFC) Systems market is experiencing robust growth, driven by the increasing need for efficient and contactless public transportation solutions globally. The market, estimated at $15 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 8% from 2025 to 2033, reaching approximately $28 billion by 2033. This expansion is fueled by several key factors. Firstly, the rising adoption of contactless payment technologies like Near-Field Communication (NFC) and mobile ticketing is streamlining fare collection processes, enhancing passenger experience, and reducing operational costs for transit agencies. Secondly, governments worldwide are investing heavily in upgrading public transportation infrastructure, fostering the demand for advanced AFC systems capable of handling large passenger volumes and integrating with various smart city initiatives. Furthermore, the growing popularity of smart cards and the increasing implementation of open-loop payment systems further contribute to market growth. Technological advancements, such as improved data analytics and integration with other transportation modes, also play a crucial role in driving market expansion.

However, the market faces certain restraints. High initial investment costs associated with deploying and maintaining AFC systems can be a barrier, particularly for smaller transit agencies in developing countries. Moreover, concerns regarding data security and privacy related to passenger information collected through these systems need to be addressed effectively. Nevertheless, the long-term benefits of improved efficiency, reduced fraud, and enhanced passenger experience outweigh these challenges, solidifying the positive outlook for the AFC systems market. Segmentation analysis reveals a strong preference for NFC technology and significant application within the transport & logistics and government sectors. Key players like Thales Group, Cubic Corporation, and others are actively driving innovation and expanding their market presence through strategic partnerships and technological advancements. Regional growth is expected to be fairly distributed, with North America and Asia Pacific representing the largest market shares, driven by the substantial investments in public transportation infrastructure and the high adoption rate of contactless payment solutions in these regions.

Automated Fare Collection Systems Trends

The global Automated Fare Collection (AFC) Systems market is experiencing robust growth, projected to reach multi-billion dollar valuations by 2033. This expansion is fueled by the increasing adoption of contactless payment technologies, the rise of smart cities, and the escalating demand for efficient and seamless public transportation. The historical period (2019-2024) witnessed significant investments in upgrading existing systems and deploying new AFC solutions across various sectors, including transport and logistics, which remains the dominant application area. The shift towards Near-Field Communication (NFC) technology is a key trend, driven by its enhanced security features, faster transaction speeds, and convenience for users. Magnetic stripe technology, while still prevalent, is gradually being replaced by more advanced solutions. The market is also witnessing diversification across different applications, with increasing adoption in areas like media and entertainment, and government services. The base year 2025 shows a substantial market size, and forecasts for 2025-2033 indicate continued impressive growth, particularly in developing economies undergoing rapid urbanization and infrastructure development. The estimated market value for 2025 highlights the significant investment and adoption already taking place. This report, covering the study period 2019-2033, provides a detailed analysis of these trends and their implications for market players. Key market insights include the strong preference for integrated systems that offer interoperability across different modes of transportation and the rising demand for data analytics capabilities to optimize operations and enhance passenger experience. The increasing integration of AFC systems with other smart city initiatives further strengthens the growth trajectory. Furthermore, the focus on improving cybersecurity measures within AFC systems is becoming increasingly crucial, as the amount of sensitive passenger data processed rises.

Driving Forces: What's Propelling the Automated Fare Collection Systems

Several factors are propelling the growth of the Automated Fare Collection Systems market. Firstly, the increasing urbanization globally necessitates efficient and reliable public transportation systems, and AFC systems are integral to optimizing these systems. Secondly, the rising popularity of contactless payment methods, such as NFC, enhances convenience and reduces transaction times, leading to wider adoption. Government initiatives promoting cashless transactions and the development of smart cities are further bolstering the market. These initiatives often include substantial investments in modernizing public transport infrastructure with integrated AFC systems. The continuous advancements in technology, such as improved data analytics capabilities for better resource management and optimized route planning, also contribute to market growth. Furthermore, the increasing demand for improved security and fraud prevention features in AFC systems drives innovation and investment in more sophisticated solutions. The growing need for seamless interoperability between different transport modes, allowing passengers to use a single payment method across various services, is a crucial driver of market expansion. Finally, the rising demand for real-time data and analytics for efficient service management, route optimization, and predictive maintenance further fuels market growth.

Challenges and Restraints in Automated Fare Collection Systems

Despite the significant growth potential, the Automated Fare Collection Systems market faces certain challenges. High initial investment costs for implementing and upgrading AFC systems can be a significant barrier for smaller municipalities and transit authorities, especially in developing countries. The complexity of integrating different systems and technologies across diverse transport modes and payment platforms presents another hurdle. Ensuring seamless interoperability and data security across different systems is a constant challenge. Furthermore, maintaining and updating these systems requires ongoing investment and technical expertise, which can add to the operational costs. Cybersecurity threats pose a significant risk, as AFC systems handle sensitive passenger data, making them targets for malicious attacks. Maintaining the robustness and resilience of the systems against cyberattacks is crucial. The need for robust customer support and comprehensive training for both staff and passengers is also a challenge. Addressing the digital literacy gap among some passenger segments is vital for successful adoption and to maximize the benefits of AFC systems. Finally, regulatory compliance and the need to adapt to evolving payment technologies and standards require constant updates and upgrades, contributing to the overall cost and complexity.

Key Region or Country & Segment to Dominate the Market

The Transport & Logistics application segment is projected to dominate the Automated Fare Collection Systems market throughout the forecast period (2025-2033). This is due to the significant investments made by governments and private companies in modernizing public transportation networks globally. The segment encompasses various modes of transport, including buses, trains, subways, and trams, all of which require robust and reliable AFC systems. The rising popularity of mass transit solutions, driven by factors like urbanization and environmental concerns, significantly contributes to this segment's dominance.

- North America and Europe: These regions are expected to maintain a strong market share due to advanced infrastructure, high technology adoption rates, and strong governmental support for smart city initiatives.

- Asia-Pacific: This region is projected to witness the fastest growth rate due to rapid urbanization, expanding public transport networks, and rising disposable incomes. Countries like China and India are at the forefront of AFC system deployment.

- Near-Field Communication (NFC) Technology: This segment is rapidly gaining traction due to its ease of use, enhanced security features, and compatibility with mobile payment solutions. NFC offers faster transaction processing times compared to older technologies, and its integration with mobile wallets and smartphones adds to its appeal for passengers.

The dominance of the Transport & Logistics segment is further solidified by the increasing focus on integrated ticketing systems that provide seamless travel across multiple transport modes. This requires sophisticated AFC infrastructure capable of handling diverse payment methods and data exchange. The demand for real-time data analytics to optimize operations and enhance the passenger experience also contributes to the growth of this segment. The continued advancements in NFC technology and the growing adoption of contactless payment solutions are projected to further strengthen the position of the Transport & Logistics segment in the global Automated Fare Collection Systems market.

Growth Catalysts in Automated Fare Collection Systems Industry

Several factors act as growth catalysts for the AFC systems industry. The increasing adoption of smart city initiatives is driving demand for integrated and technologically advanced AFC solutions. Governments globally are investing heavily in improving public transportation efficiency, which necessitates the deployment of modern AFC systems. The rising popularity of contactless payments and mobile wallets is fueling the demand for NFC-based AFC systems, offering faster and more secure transactions. Furthermore, ongoing technological advancements, particularly in areas such as data analytics and cybersecurity, contribute to market growth. These improvements enhance system performance, security, and operational efficiency. Improved passenger experience through streamlined payment processes and integration with other smart city services further encourages market expansion.

Leading Players in the Automated Fare Collection Systems

- Advanced Card Systems Holdings

- Thales Group

- Omron

- Vix Technology

- Samsung

- LG Corp

- GMV

- Cubic Corporation

- Atos SE

- Scheidt & Bachmann GmbH

- Singapore Technologies

Significant Developments in Automated Fare Collection Systems Sector

- 2020: Cubic Corporation launched a new mobile ticketing solution for public transportation.

- 2021: Advanced Card Systems Holdings released an upgraded NFC reader for AFC systems.

- 2022: Several cities implemented large-scale upgrades to their AFC systems, integrating NFC and mobile payment options.

- 2023: Thales Group partnered with a major transit authority to deploy a new integrated AFC system.

Comprehensive Coverage Automated Fare Collection Systems Report

This report provides a comprehensive overview of the Automated Fare Collection Systems market, analyzing key trends, drivers, challenges, and growth opportunities. It includes detailed market segmentation by type and application, regional market analysis, and competitive landscape profiling of leading industry players. The report leverages extensive data analysis and market research to provide insightful projections for market growth and identifies key technological advancements impacting the sector. It also delves into the evolving regulatory landscape and its influence on market dynamics. The report aims to serve as a valuable resource for stakeholders including industry professionals, investors, and researchers seeking a thorough understanding of this rapidly evolving market.

Automated Fare Collection Systems Segmentation

-

1. Type

- 1.1. Near-Field Communication

- 1.2. Magnetic Stripes

- 1.3. OCR

- 1.4. Smart Card

- 1.5. Other

-

2. Application

- 2.1. Transport & Logistic

- 2.2. Media & Entertainment

- 2.3. Government

- 2.4. Retail

- 2.5. Other

Automated Fare Collection Systems Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Automated Fare Collection Systems REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automated Fare Collection Systems Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Near-Field Communication

- 5.1.2. Magnetic Stripes

- 5.1.3. OCR

- 5.1.4. Smart Card

- 5.1.5. Other

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Transport & Logistic

- 5.2.2. Media & Entertainment

- 5.2.3. Government

- 5.2.4. Retail

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Automated Fare Collection Systems Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Near-Field Communication

- 6.1.2. Magnetic Stripes

- 6.1.3. OCR

- 6.1.4. Smart Card

- 6.1.5. Other

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Transport & Logistic

- 6.2.2. Media & Entertainment

- 6.2.3. Government

- 6.2.4. Retail

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. South America Automated Fare Collection Systems Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Near-Field Communication

- 7.1.2. Magnetic Stripes

- 7.1.3. OCR

- 7.1.4. Smart Card

- 7.1.5. Other

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Transport & Logistic

- 7.2.2. Media & Entertainment

- 7.2.3. Government

- 7.2.4. Retail

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Automated Fare Collection Systems Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Near-Field Communication

- 8.1.2. Magnetic Stripes

- 8.1.3. OCR

- 8.1.4. Smart Card

- 8.1.5. Other

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Transport & Logistic

- 8.2.2. Media & Entertainment

- 8.2.3. Government

- 8.2.4. Retail

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East & Africa Automated Fare Collection Systems Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Near-Field Communication

- 9.1.2. Magnetic Stripes

- 9.1.3. OCR

- 9.1.4. Smart Card

- 9.1.5. Other

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Transport & Logistic

- 9.2.2. Media & Entertainment

- 9.2.3. Government

- 9.2.4. Retail

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific Automated Fare Collection Systems Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Near-Field Communication

- 10.1.2. Magnetic Stripes

- 10.1.3. OCR

- 10.1.4. Smart Card

- 10.1.5. Other

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Transport & Logistic

- 10.2.2. Media & Entertainment

- 10.2.3. Government

- 10.2.4. Retail

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Advanced Card Systems Holdings

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Thales Group

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Omron

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Vix Technology

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Samsung

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 LG Corp

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 GMV

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Cubic Corporation

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Atos SE

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Scheidt & Bachmann GmbH

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Singapore Technologies

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 Advanced Card Systems Holdings

- Figure 1: Global Automated Fare Collection Systems Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Automated Fare Collection Systems Revenue (million), by Type 2024 & 2032

- Figure 3: North America Automated Fare Collection Systems Revenue Share (%), by Type 2024 & 2032

- Figure 4: North America Automated Fare Collection Systems Revenue (million), by Application 2024 & 2032

- Figure 5: North America Automated Fare Collection Systems Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Automated Fare Collection Systems Revenue (million), by Country 2024 & 2032

- Figure 7: North America Automated Fare Collection Systems Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Automated Fare Collection Systems Revenue (million), by Type 2024 & 2032

- Figure 9: South America Automated Fare Collection Systems Revenue Share (%), by Type 2024 & 2032

- Figure 10: South America Automated Fare Collection Systems Revenue (million), by Application 2024 & 2032

- Figure 11: South America Automated Fare Collection Systems Revenue Share (%), by Application 2024 & 2032

- Figure 12: South America Automated Fare Collection Systems Revenue (million), by Country 2024 & 2032

- Figure 13: South America Automated Fare Collection Systems Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Automated Fare Collection Systems Revenue (million), by Type 2024 & 2032

- Figure 15: Europe Automated Fare Collection Systems Revenue Share (%), by Type 2024 & 2032

- Figure 16: Europe Automated Fare Collection Systems Revenue (million), by Application 2024 & 2032

- Figure 17: Europe Automated Fare Collection Systems Revenue Share (%), by Application 2024 & 2032

- Figure 18: Europe Automated Fare Collection Systems Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Automated Fare Collection Systems Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Automated Fare Collection Systems Revenue (million), by Type 2024 & 2032

- Figure 21: Middle East & Africa Automated Fare Collection Systems Revenue Share (%), by Type 2024 & 2032

- Figure 22: Middle East & Africa Automated Fare Collection Systems Revenue (million), by Application 2024 & 2032

- Figure 23: Middle East & Africa Automated Fare Collection Systems Revenue Share (%), by Application 2024 & 2032

- Figure 24: Middle East & Africa Automated Fare Collection Systems Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Automated Fare Collection Systems Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Automated Fare Collection Systems Revenue (million), by Type 2024 & 2032

- Figure 27: Asia Pacific Automated Fare Collection Systems Revenue Share (%), by Type 2024 & 2032

- Figure 28: Asia Pacific Automated Fare Collection Systems Revenue (million), by Application 2024 & 2032

- Figure 29: Asia Pacific Automated Fare Collection Systems Revenue Share (%), by Application 2024 & 2032

- Figure 30: Asia Pacific Automated Fare Collection Systems Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Automated Fare Collection Systems Revenue Share (%), by Country 2024 & 2032

- Table 1: Global Automated Fare Collection Systems Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Automated Fare Collection Systems Revenue million Forecast, by Type 2019 & 2032

- Table 3: Global Automated Fare Collection Systems Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Automated Fare Collection Systems Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Automated Fare Collection Systems Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Automated Fare Collection Systems Revenue million Forecast, by Application 2019 & 2032

- Table 7: Global Automated Fare Collection Systems Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Automated Fare Collection Systems Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Automated Fare Collection Systems Revenue million Forecast, by Application 2019 & 2032

- Table 13: Global Automated Fare Collection Systems Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Automated Fare Collection Systems Revenue million Forecast, by Type 2019 & 2032

- Table 18: Global Automated Fare Collection Systems Revenue million Forecast, by Application 2019 & 2032

- Table 19: Global Automated Fare Collection Systems Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Automated Fare Collection Systems Revenue million Forecast, by Type 2019 & 2032

- Table 30: Global Automated Fare Collection Systems Revenue million Forecast, by Application 2019 & 2032

- Table 31: Global Automated Fare Collection Systems Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Automated Fare Collection Systems Revenue million Forecast, by Type 2019 & 2032

- Table 39: Global Automated Fare Collection Systems Revenue million Forecast, by Application 2019 & 2032

- Table 40: Global Automated Fare Collection Systems Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Automated Fare Collection Systems Revenue (million) Forecast, by Application 2019 & 2032

STEP 1 - Identification of Relevant Samples Size from Population Database

STEP 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note* : In applicable scenarios

STEP 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

STEP 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

Frequently Asked Questions

Related Reports

About Market Research Forecast

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.