Cloud Container Engine

Cloud Container EngineCloud Container Engine Decade Long Trends, Analysis and Forecast 2025-2033

Cloud Container Engine by Type (Public Cloud, Private Cloud, Hybrid Cloud), by Application (Large Enterprises, SMEs), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

Cloud Container Engine Decade Long Trends, Analysis and Forecast 2025-2033

Key Insights

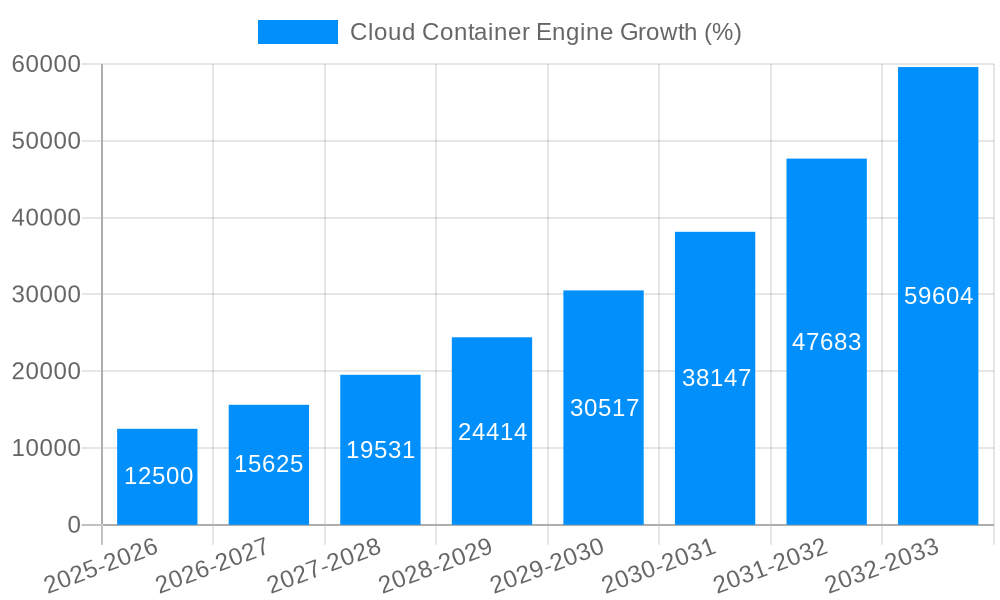

The Cloud Container Engine market is experiencing robust growth, driven by the increasing adoption of microservices architecture, the need for enhanced scalability and agility, and the rise of DevOps practices. The market, estimated at $50 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 25% from 2025 to 2033, reaching approximately $250 billion by 2033. This expansion is fueled by several key trends, including the proliferation of cloud-native applications, the growing demand for improved application portability, and the increasing focus on automation and orchestration. Large enterprises are currently the dominant segment, leveraging container engines to modernize their infrastructure and improve operational efficiency. However, the Small and Medium-sized Enterprises (SME) segment is poised for significant growth, driven by the accessibility and cost-effectiveness of cloud-based solutions. The hybrid cloud deployment model is gaining traction, enabling businesses to balance the benefits of public and private cloud environments. Geographic distribution shows strong growth across North America and Asia Pacific, with the latter region witnessing particularly rapid expansion due to the burgeoning tech sector in China and India. Competitive pressures are intense, with major players like Google, Microsoft, Amazon (implied although not explicitly listed), and Alibaba fiercely vying for market share through continuous innovation and strategic partnerships. Restraints to growth include concerns around security, lack of skilled professionals, and the complexity associated with managing containerized environments.

The competitive landscape features a mix of established cloud providers and specialized container orchestration platform providers. Key players are aggressively investing in research and development to enhance their offerings, including improved security features, enhanced management tools, and better integration with existing cloud infrastructure. Furthermore, strategic acquisitions and partnerships are common strategies employed to expand market reach and bolster product capabilities. The market's future trajectory suggests continued dominance by major players, although emerging niche players focusing on specialized solutions or specific industry verticals may carve out profitable segments. The ongoing evolution of containerization technologies and the increasing demand for robust and secure container management platforms ensures substantial market growth throughout the forecast period.

Cloud Container Engine Trends

The global cloud container engine market is experiencing explosive growth, projected to reach multi-million dollar valuations by 2033. Driven by the increasing adoption of microservices architectures and the need for agile and scalable applications, the market witnessed significant expansion during the historical period (2019-2024). The estimated market value in 2025 sits at several million dollars, reflecting a robust compound annual growth rate (CAGR) throughout the forecast period (2025-2033). This growth is fueled by a confluence of factors, including the rising demand for container orchestration platforms like Kubernetes, the maturation of serverless computing, and the expansion of cloud-native application development. Key market insights reveal a strong preference for public cloud deployments, particularly amongst large enterprises seeking to leverage the scalability and cost-effectiveness offered by leading providers. However, the private and hybrid cloud segments are also exhibiting healthy growth, driven by increasing concerns about data security and regulatory compliance. Small and medium-sized enterprises (SMEs) are increasingly adopting containerization technologies, albeit at a slower pace than large enterprises, primarily due to budgetary constraints and a lack of in-house expertise. The competition among major cloud providers is intense, pushing innovation and driving down prices, making cloud container engine solutions more accessible across various industries. This competitive landscape encourages continuous improvement and the development of specialized solutions tailored to particular industry needs. The base year for our analysis is 2025, providing a crucial benchmark against which future growth can be measured and compared.

Driving Forces: What's Propelling the Cloud Container Engine

Several powerful forces are propelling the expansion of the cloud container engine market. Firstly, the widespread adoption of microservices architecture is a major catalyst. Microservices' inherent modularity and independent deployability perfectly align with the containerization paradigm, allowing for faster development cycles, improved scalability, and enhanced fault isolation. Secondly, the increasing popularity of DevOps methodologies and continuous integration/continuous delivery (CI/CD) pipelines fuels the demand for containerization solutions. Containers streamline the deployment and management of applications across diverse environments, enabling faster releases and improved operational efficiency. The rise of cloud-native applications, designed specifically to run in cloud environments, is another critical driver. These applications inherently leverage containers and orchestration platforms to achieve scalability, resilience, and cost optimization. Furthermore, the increasing complexity of applications and the need for seamless integration across various cloud services necessitate robust container management solutions. Finally, the growing focus on automation and infrastructure as code further contributes to the market's growth, simplifying deployment, management, and scaling of containerized applications. These interconnected trends create a powerful synergy driving the rapid adoption of cloud container engine technology across a range of industries and organizations.

Challenges and Restraints in Cloud Container Engine

Despite the significant growth potential, the cloud container engine market faces several challenges and restraints. Security remains a paramount concern, with vulnerabilities in container images and orchestration platforms posing a significant risk. Ensuring the security of containerized applications requires robust security practices and tools throughout the entire application lifecycle. The complexity of managing and monitoring containerized environments can also be a deterrent, especially for organizations lacking the necessary expertise. Skill shortages in DevOps and cloud-native technologies create a significant hurdle for widespread adoption, particularly within SMEs. The integration of containerization with existing legacy systems can also prove challenging and costly, hindering the migration of applications to cloud-native architectures. Furthermore, the ongoing evolution of container technologies and orchestration platforms necessitates continuous learning and adaptation, requiring significant investment in training and development. Finally, vendor lock-in poses a potential risk, as organizations may find it difficult to migrate their applications between different cloud providers or platforms. Addressing these challenges will be crucial for ensuring the continued growth and widespread adoption of cloud container engine technologies.

Key Region or Country & Segment to Dominate the Market

The public cloud segment is projected to dominate the market throughout the forecast period. This dominance is attributed to its inherent scalability, cost-effectiveness, and ease of use, particularly appealing to large enterprises. Public cloud providers offer a wide array of services and features, including managed Kubernetes services, facilitating faster deployment and reduced operational overhead.

North America and Western Europe are expected to be leading regions due to the high concentration of large enterprises, strong technological infrastructure, and early adoption of cloud technologies. These regions benefit from a highly skilled workforce and a culture of innovation, further accelerating the growth of public cloud container engine adoption.

Large Enterprises represent a significant market segment, driving a substantial portion of the demand for sophisticated container orchestration and management solutions. These organizations possess the resources and expertise to fully leverage the benefits of public cloud container engines, achieving greater scalability, agility, and efficiency. Their willingness to invest in robust infrastructure and skilled personnel accelerates the deployment of containerized applications and associated services.

While the private cloud segment shows significant growth, primarily driven by organizations with stringent security requirements or specific compliance regulations, the public cloud's flexibility and cost-effectiveness make it the more dominant force. The hybrid cloud segment occupies a niche position, catering to organizations seeking a balance between the benefits of public and private cloud deployments. SMEs' adoption of cloud container engines lags behind large enterprises, primarily due to their limited budgets and lack of expertise.

In summary, the public cloud segment, particularly in North America and Western Europe, with large enterprises as the primary driver, will lead the market in terms of revenue generation and growth. The massive investments made by leading cloud providers further strengthen this projection, reinforcing the public cloud's position as the dominant force in the cloud container engine market during 2025-2033.

Growth Catalysts in Cloud Container Engine Industry

The cloud container engine market's growth is significantly boosted by several key factors. Increased investments in research and development by major technology companies are leading to innovative solutions and enhanced capabilities. The growing adoption of microservices architectures and DevOps methodologies is significantly fueling market expansion, while strong government support for digital transformation initiatives is further encouraging the widespread adoption of containerization technologies. These interconnected factors create a virtuous cycle, driving innovation and accelerating the growth of the market as a whole.

Leading Players in the Cloud Container Engine

- HUAWEI

- T-Systems International

- Oracle

- Orange Business Services

- SberCloud

- IBM

- Baidu

- Alibaba

- Tencent

- Mirantis

- Microsoft

Significant Developments in Cloud Container Engine Sector

- 2020: Kubernetes 1.20 released, introducing significant improvements in scalability and security.

- 2021: Increased adoption of serverless container platforms.

- 2022: Focus on enhancing security and compliance features within container orchestration platforms.

- 2023: Significant advancements in AI-powered container management tools.

- 2024: Growing integration of container technologies with edge computing.

Comprehensive Coverage Cloud Container Engine Report

This report provides a comprehensive overview of the cloud container engine market, covering key trends, driving forces, challenges, and growth catalysts. It offers detailed analysis of major market segments, including public, private, and hybrid cloud deployments, and assesses the market performance across key geographical regions. The report also features profiles of leading players in the industry, providing insights into their strategies, market share, and future outlook. The data presented within offers a robust forecast for the market's trajectory through 2033.

Cloud Container Engine Segmentation

-

1. Type

- 1.1. Public Cloud

- 1.2. Private Cloud

- 1.3. Hybrid Cloud

-

2. Application

- 2.1. Large Enterprises

- 2.2. SMEs

Cloud Container Engine Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cloud Container Engine REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Frequently Asked Questions

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cloud Container Engine Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Public Cloud

- 5.1.2. Private Cloud

- 5.1.3. Hybrid Cloud

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Large Enterprises

- 5.2.2. SMEs

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Cloud Container Engine Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Public Cloud

- 6.1.2. Private Cloud

- 6.1.3. Hybrid Cloud

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Large Enterprises

- 6.2.2. SMEs

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. South America Cloud Container Engine Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Public Cloud

- 7.1.2. Private Cloud

- 7.1.3. Hybrid Cloud

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Large Enterprises

- 7.2.2. SMEs

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Cloud Container Engine Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Public Cloud

- 8.1.2. Private Cloud

- 8.1.3. Hybrid Cloud

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Large Enterprises

- 8.2.2. SMEs

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East & Africa Cloud Container Engine Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Public Cloud

- 9.1.2. Private Cloud

- 9.1.3. Hybrid Cloud

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Large Enterprises

- 9.2.2. SMEs

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific Cloud Container Engine Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Public Cloud

- 10.1.2. Private Cloud

- 10.1.3. Hybrid Cloud

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Large Enterprises

- 10.2.2. SMEs

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 HUAWEI

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Google

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 T-Systems International

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Oracle

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Orange Business Services

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 SberCloud

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 IBM

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Baidu

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Alibaba

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tencent

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Mirantis

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 Microsoft

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.1 HUAWEI

- Figure 1: Global Cloud Container Engine Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Cloud Container Engine Revenue (million), by Type 2024 & 2032

- Figure 3: North America Cloud Container Engine Revenue Share (%), by Type 2024 & 2032

- Figure 4: North America Cloud Container Engine Revenue (million), by Application 2024 & 2032

- Figure 5: North America Cloud Container Engine Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Cloud Container Engine Revenue (million), by Country 2024 & 2032

- Figure 7: North America Cloud Container Engine Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Cloud Container Engine Revenue (million), by Type 2024 & 2032

- Figure 9: South America Cloud Container Engine Revenue Share (%), by Type 2024 & 2032

- Figure 10: South America Cloud Container Engine Revenue (million), by Application 2024 & 2032

- Figure 11: South America Cloud Container Engine Revenue Share (%), by Application 2024 & 2032

- Figure 12: South America Cloud Container Engine Revenue (million), by Country 2024 & 2032

- Figure 13: South America Cloud Container Engine Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Cloud Container Engine Revenue (million), by Type 2024 & 2032

- Figure 15: Europe Cloud Container Engine Revenue Share (%), by Type 2024 & 2032

- Figure 16: Europe Cloud Container Engine Revenue (million), by Application 2024 & 2032

- Figure 17: Europe Cloud Container Engine Revenue Share (%), by Application 2024 & 2032

- Figure 18: Europe Cloud Container Engine Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Cloud Container Engine Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Cloud Container Engine Revenue (million), by Type 2024 & 2032

- Figure 21: Middle East & Africa Cloud Container Engine Revenue Share (%), by Type 2024 & 2032

- Figure 22: Middle East & Africa Cloud Container Engine Revenue (million), by Application 2024 & 2032

- Figure 23: Middle East & Africa Cloud Container Engine Revenue Share (%), by Application 2024 & 2032

- Figure 24: Middle East & Africa Cloud Container Engine Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Cloud Container Engine Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Cloud Container Engine Revenue (million), by Type 2024 & 2032

- Figure 27: Asia Pacific Cloud Container Engine Revenue Share (%), by Type 2024 & 2032

- Figure 28: Asia Pacific Cloud Container Engine Revenue (million), by Application 2024 & 2032

- Figure 29: Asia Pacific Cloud Container Engine Revenue Share (%), by Application 2024 & 2032

- Figure 30: Asia Pacific Cloud Container Engine Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Cloud Container Engine Revenue Share (%), by Country 2024 & 2032

- Table 1: Global Cloud Container Engine Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Cloud Container Engine Revenue million Forecast, by Type 2019 & 2032

- Table 3: Global Cloud Container Engine Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Cloud Container Engine Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Cloud Container Engine Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Cloud Container Engine Revenue million Forecast, by Application 2019 & 2032

- Table 7: Global Cloud Container Engine Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Cloud Container Engine Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Cloud Container Engine Revenue million Forecast, by Application 2019 & 2032

- Table 13: Global Cloud Container Engine Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Cloud Container Engine Revenue million Forecast, by Type 2019 & 2032

- Table 18: Global Cloud Container Engine Revenue million Forecast, by Application 2019 & 2032

- Table 19: Global Cloud Container Engine Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Cloud Container Engine Revenue million Forecast, by Type 2019 & 2032

- Table 30: Global Cloud Container Engine Revenue million Forecast, by Application 2019 & 2032

- Table 31: Global Cloud Container Engine Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Cloud Container Engine Revenue million Forecast, by Type 2019 & 2032

- Table 39: Global Cloud Container Engine Revenue million Forecast, by Application 2019 & 2032

- Table 40: Global Cloud Container Engine Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Cloud Container Engine Revenue (million) Forecast, by Application 2019 & 2032

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

STEP 1 - Identification of Relevant Samples Size from Population Database

STEP 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note* : In applicable scenarios

STEP 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

STEP 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

Related Reports

About Market Research Forecast

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.