Cloud Firewall Management

Cloud Firewall ManagementCloud Firewall Management Strategic Insights: Analysis 2025 and Forecasts 2033

Cloud Firewall Management by Type (Managed Firewall, Managed Intrusion Detection/Prevention System, Unified Threat Management, Vulnerability Management, Compliance Management, Distributed Denial Of Service, Managed Security Information And Event Management, Identity And Access Management, Antivirus/Antimalware, Others), by Application (BFSI (Banking, Financial Services and Insurance), Government and Defense, Healthcare and Life Sciences, Telecom and IT, Retail and Consumer Packaged Goods, Energy and Utilities, Education, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

Cloud Firewall Management Strategic Insights: Analysis 2025 and Forecasts 2033

Cloud Firewall Management Strategic Insights: Analysis 2025 and Forecasts 2033

Key Insights

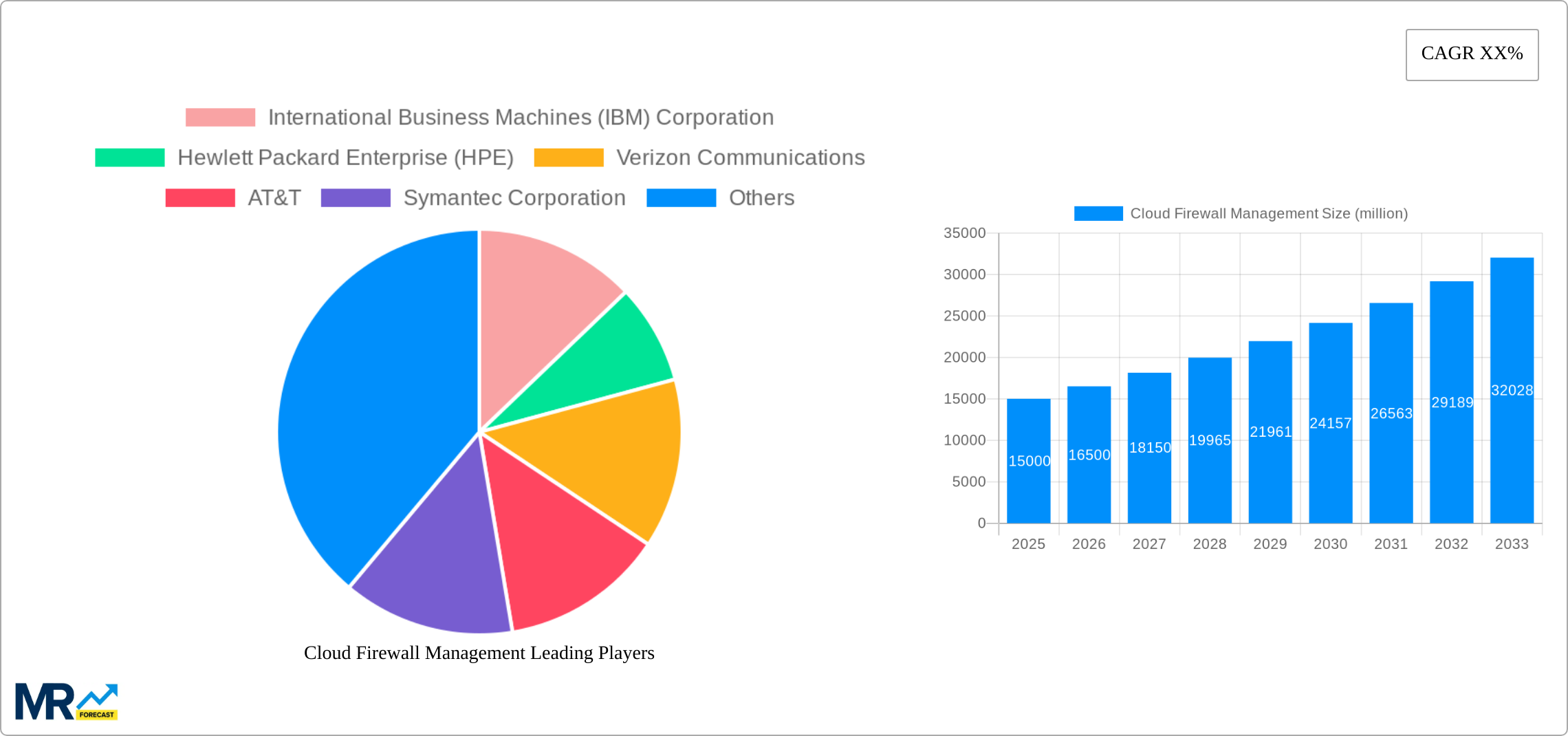

The Cloud Firewall Management market is experiencing robust growth, driven by the increasing adoption of cloud-based services and the rising need for enhanced cybersecurity measures across diverse sectors. The market's expansion is fueled by several key factors, including the escalating number of cyber threats, stringent regulatory compliance requirements (like GDPR and CCPA), and the inherent scalability and cost-effectiveness offered by cloud-based firewall solutions compared to traditional on-premise systems. The BFSI, Government & Defense, and Healthcare & Life Sciences sectors are leading the adoption, owing to their sensitive data and critical infrastructure. Growth is further accelerated by the integration of advanced functionalities like AI and machine learning into cloud firewall management platforms, enabling proactive threat detection and automated response mechanisms. While the market faces certain restraints like concerns regarding data sovereignty and vendor lock-in, the overall trend points towards sustained and significant expansion. We estimate the 2025 market size to be around $15 Billion, based on a conservative projection considering typical growth rates for similar cybersecurity segments.

The market segmentation reveals a diverse landscape, with Managed Firewall and Unified Threat Management (UTM) services currently dominating the offerings. However, the demand for more specialized solutions such as Managed Intrusion Detection/Prevention Systems (IDS/IPS), Vulnerability Management, and Identity and Access Management (IAM) is also rapidly increasing. Geographic distribution shows strong performance in North America and Europe, reflecting higher cloud adoption rates and robust cybersecurity investments in these regions. However, the Asia-Pacific region is expected to witness exponential growth in the coming years, driven by rapid digital transformation and expanding cloud infrastructure in countries like India and China. This signifies promising opportunities for market players, necessitating strategic investments in research and development, particularly focusing on AI-driven security solutions and tailored offerings for emerging markets. The competitive landscape is intensely dynamic, with established players alongside nimble startups vying for market share. Strategic partnerships and acquisitions are likely to be key strategies for both groups as they strive for dominance in this evolving environment.

Cloud Firewall Management Trends

The global cloud firewall management market is experiencing explosive growth, projected to reach tens of billions of dollars by 2033. This surge is driven by the increasing adoption of cloud computing across various sectors, alongside the escalating need for robust cybersecurity solutions. The market witnessed significant expansion during the historical period (2019-2024), exceeding several billion dollars annually in the latter years. This upward trajectory is expected to continue throughout the forecast period (2025-2033), propelled by several key factors. Businesses are increasingly migrating their IT infrastructure to the cloud for enhanced scalability, flexibility, and cost-effectiveness. However, this migration brings new security challenges, demanding sophisticated cloud-based firewall management solutions. The rising incidence of cyberattacks, targeting both large enterprises and small businesses, further fuels this demand. Moreover, stringent government regulations and industry compliance standards are mandating robust security measures, thereby driving the adoption of advanced cloud firewall management systems. Key market insights reveal a strong preference for managed services, particularly Unified Threat Management (UTM) solutions, due to their comprehensive nature and ease of implementation. The BFSI sector, owing to its high sensitivity to data breaches, remains a significant revenue driver. The market is also witnessing a gradual shift towards Artificial Intelligence (AI) and Machine Learning (ML) integrated solutions, enabling more proactive and efficient threat detection and response. The projected market value for 2025 is estimated in the tens of billions, signifying a substantial increase from previous years and setting the stage for continued, significant growth throughout the forecast period. This growth is not solely driven by increased spending but also by the expansion of cloud adoption itself, creating a consistently growing market for protective measures.

Driving Forces: What's Propelling the Cloud Firewall Management Market?

The cloud firewall management market's rapid expansion is fueled by a confluence of factors. The increasing reliance on cloud services across all industries is a primary driver. As more businesses migrate sensitive data and applications to the cloud, the need for robust security measures becomes paramount. This necessitates sophisticated firewall management systems capable of adapting to the dynamic nature of cloud environments. Furthermore, the sophistication and frequency of cyberattacks are continuously escalating, pushing organizations to invest in advanced threat prevention and mitigation technologies. Data breaches can lead to significant financial losses, reputational damage, and legal repercussions, making proactive security a critical business imperative. The growing complexity of cloud environments, characterized by multiple virtual machines, networks, and applications, further contributes to the demand for centralized and automated firewall management solutions. These solutions offer improved visibility, control, and efficiency in managing security policies across a distributed cloud infrastructure. Lastly, stringent compliance regulations and industry standards (like GDPR, HIPAA, etc.) are compelling organizations to adopt and maintain robust security practices, significantly impacting the market's growth trajectory. The increasing need to ensure data security and regulatory compliance across the enterprise and in various industries are important contributors to the growth of this market.

Challenges and Restraints in Cloud Firewall Management

Despite the significant growth potential, the cloud firewall management market faces several challenges. The complexity of cloud environments and the diversity of platforms can make the implementation and management of firewall solutions cumbersome and resource-intensive. Integrating cloud firewall systems with existing on-premise security infrastructure can pose significant technical difficulties and require substantial expertise. The ever-evolving nature of cyber threats requires constant vigilance and adaptation. Keeping up with the latest threats and vulnerabilities necessitates continuous updates and improvements to firewall configurations and security policies. This requires significant ongoing investment in skilled personnel, training, and software updates. Cost can also be a significant barrier, especially for smaller businesses with limited budgets. The cost of implementing and maintaining advanced cloud firewall management systems, including licensing fees, ongoing maintenance, and skilled personnel, can be substantial. Furthermore, the scarcity of skilled cybersecurity professionals capable of managing and maintaining these complex systems creates a significant bottleneck. The market also faces challenges regarding effective management of multi-cloud environments, especially when dealing with the nuances of different cloud providers' security models.

Key Region or Country & Segment to Dominate the Market

North America: This region is expected to maintain its dominant position, driven by high cloud adoption rates, strong cybersecurity awareness, and a substantial presence of major technology companies and cloud service providers. The region's robust regulatory framework and stringent compliance requirements further propel the market's growth. The high concentration of businesses in various sectors (BFSI, Government, Healthcare) needing robust security solutions contributes to this dominance.

Europe: Growing regulatory compliance demands, particularly driven by the GDPR, are pushing organizations in this region to prioritize strong cloud security measures. Increased adoption of cloud services and an increasing awareness of cyber threats across various sectors is driving this market expansion. The market shows steady growth, expected to maintain a substantial share of the global market in the coming years.

Asia-Pacific: This region is witnessing rapid growth due to increasing digitalization, cloud adoption, and rising cybersecurity concerns. The region's burgeoning economies and expanding technological landscape are creating considerable opportunities for cloud firewall management providers. The rapid increase in mobile device adoption and digital transformation initiatives further fuel market growth. Government support for digital infrastructure expansion also serves as a catalyst for this growth.

Managed Firewall Segment: This segment is currently the largest within the market due to its scalability, ease of management, and cost-effectiveness compared to self-managed solutions. Organizations are opting for this as a strategic move towards optimizing operational efficiency and improving their threat response capabilities. The shift towards cloud-native solutions also complements the attractiveness of this segment.

BFSI Application Segment: This sector's stringent compliance requirements and its high sensitivity to data breaches are key drivers for the segment's remarkable growth. Banks and financial institutions are continuously improving their security posture, investing heavily in sophisticated cloud firewall management systems to safeguard customer data and comply with regulations. This segment is projected to continue this strong growth trajectory throughout the forecast period.

The paragraph above explains the dominance of these regions and segments with additional details.

Growth Catalysts in the Cloud Firewall Management Industry

Several factors are driving growth in the cloud firewall management industry. The rise of hybrid and multi-cloud environments necessitates solutions that can seamlessly manage security across multiple platforms. Furthermore, advancements in AI and ML are leading to more sophisticated threat detection and response capabilities, improving the effectiveness of cloud firewall management systems. The increasing adoption of DevOps methodologies also necessitates integrated security solutions capable of automating security processes and accelerating deployment cycles. These factors, along with growing awareness of data privacy regulations, contribute to a robust and consistently growing market for cloud firewall management systems.

Leading Players in the Cloud Firewall Management Market

- International Business Machines (IBM) Corporation

- Hewlett Packard Enterprise (HPE)

- Verizon Communications

- AT&T

- Symantec Corporation

- Fortinet

- Solutionary

- Secureworks

- Computer Sciences Corporations

- Centurylink

Significant Developments in the Cloud Firewall Management Sector

- 2020: Increased adoption of cloud-native firewall solutions.

- 2021: Significant investment in AI-powered threat detection systems.

- 2022: Rise of cloud-based Secure Access Service Edge (SASE) solutions.

- 2023: Growing integration of cloud firewall management with DevSecOps practices.

- 2024: Expansion of Zero Trust security architectures.

Comprehensive Coverage Cloud Firewall Management Report

This report provides a detailed analysis of the cloud firewall management market, covering market trends, driving forces, challenges, key players, and significant developments. It offers insights into the growth trajectory of various segments and regions, providing valuable information for stakeholders seeking to understand and navigate this rapidly evolving market landscape. The report's comprehensive coverage includes detailed market sizing and forecasting, supported by robust methodologies and data. This provides a thorough understanding of the competitive dynamics and investment opportunities within the industry.

Cloud Firewall Management Segmentation

-

1. Type

- 1.1. Managed Firewall

- 1.2. Managed Intrusion Detection/Prevention System

- 1.3. Unified Threat Management

- 1.4. Vulnerability Management

- 1.5. Compliance Management

- 1.6. Distributed Denial Of Service

- 1.7. Managed Security Information And Event Management

- 1.8. Identity And Access Management

- 1.9. Antivirus/Antimalware

- 1.10. Others

-

2. Application

- 2.1. BFSI (Banking, Financial Services and Insurance)

- 2.2. Government and Defense

- 2.3. Healthcare and Life Sciences

- 2.4. Telecom and IT

- 2.5. Retail and Consumer Packaged Goods

- 2.6. Energy and Utilities

- 2.7. Education

- 2.8. Others

Cloud Firewall Management Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Cloud Firewall Management REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Cloud Firewall Management Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Managed Firewall

- 5.1.2. Managed Intrusion Detection/Prevention System

- 5.1.3. Unified Threat Management

- 5.1.4. Vulnerability Management

- 5.1.5. Compliance Management

- 5.1.6. Distributed Denial Of Service

- 5.1.7. Managed Security Information And Event Management

- 5.1.8. Identity And Access Management

- 5.1.9. Antivirus/Antimalware

- 5.1.10. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. BFSI (Banking, Financial Services and Insurance)

- 5.2.2. Government and Defense

- 5.2.3. Healthcare and Life Sciences

- 5.2.4. Telecom and IT

- 5.2.5. Retail and Consumer Packaged Goods

- 5.2.6. Energy and Utilities

- 5.2.7. Education

- 5.2.8. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Cloud Firewall Management Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Managed Firewall

- 6.1.2. Managed Intrusion Detection/Prevention System

- 6.1.3. Unified Threat Management

- 6.1.4. Vulnerability Management

- 6.1.5. Compliance Management

- 6.1.6. Distributed Denial Of Service

- 6.1.7. Managed Security Information And Event Management

- 6.1.8. Identity And Access Management

- 6.1.9. Antivirus/Antimalware

- 6.1.10. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. BFSI (Banking, Financial Services and Insurance)

- 6.2.2. Government and Defense

- 6.2.3. Healthcare and Life Sciences

- 6.2.4. Telecom and IT

- 6.2.5. Retail and Consumer Packaged Goods

- 6.2.6. Energy and Utilities

- 6.2.7. Education

- 6.2.8. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. South America Cloud Firewall Management Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Managed Firewall

- 7.1.2. Managed Intrusion Detection/Prevention System

- 7.1.3. Unified Threat Management

- 7.1.4. Vulnerability Management

- 7.1.5. Compliance Management

- 7.1.6. Distributed Denial Of Service

- 7.1.7. Managed Security Information And Event Management

- 7.1.8. Identity And Access Management

- 7.1.9. Antivirus/Antimalware

- 7.1.10. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. BFSI (Banking, Financial Services and Insurance)

- 7.2.2. Government and Defense

- 7.2.3. Healthcare and Life Sciences

- 7.2.4. Telecom and IT

- 7.2.5. Retail and Consumer Packaged Goods

- 7.2.6. Energy and Utilities

- 7.2.7. Education

- 7.2.8. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Cloud Firewall Management Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Managed Firewall

- 8.1.2. Managed Intrusion Detection/Prevention System

- 8.1.3. Unified Threat Management

- 8.1.4. Vulnerability Management

- 8.1.5. Compliance Management

- 8.1.6. Distributed Denial Of Service

- 8.1.7. Managed Security Information And Event Management

- 8.1.8. Identity And Access Management

- 8.1.9. Antivirus/Antimalware

- 8.1.10. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. BFSI (Banking, Financial Services and Insurance)

- 8.2.2. Government and Defense

- 8.2.3. Healthcare and Life Sciences

- 8.2.4. Telecom and IT

- 8.2.5. Retail and Consumer Packaged Goods

- 8.2.6. Energy and Utilities

- 8.2.7. Education

- 8.2.8. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East & Africa Cloud Firewall Management Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Managed Firewall

- 9.1.2. Managed Intrusion Detection/Prevention System

- 9.1.3. Unified Threat Management

- 9.1.4. Vulnerability Management

- 9.1.5. Compliance Management

- 9.1.6. Distributed Denial Of Service

- 9.1.7. Managed Security Information And Event Management

- 9.1.8. Identity And Access Management

- 9.1.9. Antivirus/Antimalware

- 9.1.10. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. BFSI (Banking, Financial Services and Insurance)

- 9.2.2. Government and Defense

- 9.2.3. Healthcare and Life Sciences

- 9.2.4. Telecom and IT

- 9.2.5. Retail and Consumer Packaged Goods

- 9.2.6. Energy and Utilities

- 9.2.7. Education

- 9.2.8. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific Cloud Firewall Management Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Managed Firewall

- 10.1.2. Managed Intrusion Detection/Prevention System

- 10.1.3. Unified Threat Management

- 10.1.4. Vulnerability Management

- 10.1.5. Compliance Management

- 10.1.6. Distributed Denial Of Service

- 10.1.7. Managed Security Information And Event Management

- 10.1.8. Identity And Access Management

- 10.1.9. Antivirus/Antimalware

- 10.1.10. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. BFSI (Banking, Financial Services and Insurance)

- 10.2.2. Government and Defense

- 10.2.3. Healthcare and Life Sciences

- 10.2.4. Telecom and IT

- 10.2.5. Retail and Consumer Packaged Goods

- 10.2.6. Energy and Utilities

- 10.2.7. Education

- 10.2.8. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 International Business Machines (IBM) Corporation

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Hewlett Packard Enterprise (HPE)

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Verizon Communications

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 AT&T

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Symantec Corporation

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Fortinet

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Solutionary

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Secureworks

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Computer Sciences Corporations

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Centurylink

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 International Business Machines (IBM) Corporation

- Figure 1: Global Cloud Firewall Management Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Cloud Firewall Management Revenue (million), by Type 2024 & 2032

- Figure 3: North America Cloud Firewall Management Revenue Share (%), by Type 2024 & 2032

- Figure 4: North America Cloud Firewall Management Revenue (million), by Application 2024 & 2032

- Figure 5: North America Cloud Firewall Management Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Cloud Firewall Management Revenue (million), by Country 2024 & 2032

- Figure 7: North America Cloud Firewall Management Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Cloud Firewall Management Revenue (million), by Type 2024 & 2032

- Figure 9: South America Cloud Firewall Management Revenue Share (%), by Type 2024 & 2032

- Figure 10: South America Cloud Firewall Management Revenue (million), by Application 2024 & 2032

- Figure 11: South America Cloud Firewall Management Revenue Share (%), by Application 2024 & 2032

- Figure 12: South America Cloud Firewall Management Revenue (million), by Country 2024 & 2032

- Figure 13: South America Cloud Firewall Management Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Cloud Firewall Management Revenue (million), by Type 2024 & 2032

- Figure 15: Europe Cloud Firewall Management Revenue Share (%), by Type 2024 & 2032

- Figure 16: Europe Cloud Firewall Management Revenue (million), by Application 2024 & 2032

- Figure 17: Europe Cloud Firewall Management Revenue Share (%), by Application 2024 & 2032

- Figure 18: Europe Cloud Firewall Management Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Cloud Firewall Management Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Cloud Firewall Management Revenue (million), by Type 2024 & 2032

- Figure 21: Middle East & Africa Cloud Firewall Management Revenue Share (%), by Type 2024 & 2032

- Figure 22: Middle East & Africa Cloud Firewall Management Revenue (million), by Application 2024 & 2032

- Figure 23: Middle East & Africa Cloud Firewall Management Revenue Share (%), by Application 2024 & 2032

- Figure 24: Middle East & Africa Cloud Firewall Management Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Cloud Firewall Management Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Cloud Firewall Management Revenue (million), by Type 2024 & 2032

- Figure 27: Asia Pacific Cloud Firewall Management Revenue Share (%), by Type 2024 & 2032

- Figure 28: Asia Pacific Cloud Firewall Management Revenue (million), by Application 2024 & 2032

- Figure 29: Asia Pacific Cloud Firewall Management Revenue Share (%), by Application 2024 & 2032

- Figure 30: Asia Pacific Cloud Firewall Management Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Cloud Firewall Management Revenue Share (%), by Country 2024 & 2032

- Table 1: Global Cloud Firewall Management Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Cloud Firewall Management Revenue million Forecast, by Type 2019 & 2032

- Table 3: Global Cloud Firewall Management Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Cloud Firewall Management Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Cloud Firewall Management Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Cloud Firewall Management Revenue million Forecast, by Application 2019 & 2032

- Table 7: Global Cloud Firewall Management Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Cloud Firewall Management Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Cloud Firewall Management Revenue million Forecast, by Application 2019 & 2032

- Table 13: Global Cloud Firewall Management Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Cloud Firewall Management Revenue million Forecast, by Type 2019 & 2032

- Table 18: Global Cloud Firewall Management Revenue million Forecast, by Application 2019 & 2032

- Table 19: Global Cloud Firewall Management Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Cloud Firewall Management Revenue million Forecast, by Type 2019 & 2032

- Table 30: Global Cloud Firewall Management Revenue million Forecast, by Application 2019 & 2032

- Table 31: Global Cloud Firewall Management Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Cloud Firewall Management Revenue million Forecast, by Type 2019 & 2032

- Table 39: Global Cloud Firewall Management Revenue million Forecast, by Application 2019 & 2032

- Table 40: Global Cloud Firewall Management Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Cloud Firewall Management Revenue (million) Forecast, by Application 2019 & 2032

STEP 1 - Identification of Relevant Samples Size from Population Database

STEP 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note* : In applicable scenarios

STEP 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

STEP 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

Frequently Asked Questions

Related Reports

About Market Research Forecast

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.