CVO Credentialing Services

CVO Credentialing ServicesCVO Credentialing Services Navigating Dynamics Comprehensive Analysis and Forecasts 2025-2033

CVO Credentialing Services by Application (Clinics, Hospitals, DME Companies, Home Health Agencies, Others), by Type (Initial and Re-credentialing, Expirables Management, Sanctions Monitoring), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

Base Year: 2024

111 Pages

CVO Credentialing Services Navigating Dynamics Comprehensive Analysis and Forecasts 2025-2033

Key Insights

The CVO (Credentialing Verification Organization) credentialing services market is experiencing robust growth, driven by increasing regulatory scrutiny, a rising need for streamlined provider enrollment processes, and the expanding adoption of electronic health records (EHRs). The market, estimated at $2.5 billion in 2025, is projected to exhibit a compound annual growth rate (CAGR) of 12% from 2025 to 2033, reaching an estimated $7.2 billion by 2033. This expansion is fueled by several key factors. Firstly, healthcare providers face increasingly complex credentialing requirements, necessitating specialized services to ensure compliance and avoid penalties. Secondly, the demand for efficient and accurate credentialing is soaring as healthcare organizations strive to optimize operational efficiency and reduce administrative burdens. Thirdly, the shift towards value-based care further emphasizes the importance of verified provider credentials, contributing to market growth. The market is segmented by application (clinics, hospitals, DME companies, home health agencies, others) and type of service (initial and re-credentialing, expirable management, sanctions monitoring). Hospitals and clinics represent the largest segments, driven by their high volume of provider onboarding and ongoing compliance needs. Initial credentialing services currently hold a larger market share compared to re-credentialing; however, re-credentialing is projected to witness faster growth due to the continuous need for updates and verification. North America currently dominates the market, followed by Europe and Asia Pacific, reflecting higher regulatory stringency and healthcare spending in these regions.

Competition within the CVO credentialing services market is intense, with a mix of large established players and emerging specialized firms. Key players such as VerityStream, symplr, and ProviderTrust are actively investing in technological advancements and strategic partnerships to enhance their service offerings and expand their market reach. Future growth will depend on continuous innovation in technology (e.g., AI-driven automation, blockchain for secure data management), an increased focus on data analytics to offer predictive insights into compliance risks, and strategic acquisitions to expand service portfolios and geographical reach. The market also faces some restraints, including high initial implementation costs for healthcare organizations and the ongoing need for skilled professionals to manage complex credentialing processes. Nevertheless, the overall outlook for the CVO credentialing services market remains positive, driven by the enduring need for efficient, reliable, and compliant provider credentialing solutions within the ever-evolving healthcare landscape.

CVO Credentialing Services Trends

The CVO (Credentialing Verification Organization) credentialing services market is experiencing robust growth, projected to reach multi-million dollar valuations by 2033. The study period from 2019 to 2033 reveals a significant upward trajectory, driven by increasing regulatory scrutiny, a rising volume of healthcare providers needing credentialing, and the inherent complexities of managing provider data across diverse healthcare settings. The base year of 2025, and the estimated year of 2025, both highlight a market already demonstrating substantial size in the millions. The forecast period from 2025 to 2033 anticipates further expansion, fueled by technological advancements and the increasing demand for streamlined, efficient credentialing processes. Historical data from 2019-2024 provides a solid foundation for understanding the market's consistent growth, highlighting the sector's resilience and attractiveness for investment. This growth is not uniform across all segments; some segments, such as hospital credentialing and re-credentialing services, are showing particularly strong growth rates compared to others. The market is becoming increasingly competitive, with both established players and new entrants vying for market share. This competitive landscape is pushing innovation and driving down costs, benefiting healthcare providers. Furthermore, the evolving regulatory environment continues to shape the market, prompting providers to seek out reliable and compliant CVO services to ensure compliance and avoid potential penalties. Overall, the market demonstrates strong potential for continued growth, driven by fundamental market shifts and technological advancements.

Driving Forces: What's Propelling the CVO Credentialing Services Market?

Several key factors are propelling the growth of the CVO credentialing services market. The increasing complexity of regulatory requirements and compliance mandates across various healthcare settings is a major driver. Healthcare providers face significant challenges in navigating the intricate web of rules and regulations surrounding provider credentialing, making specialized CVO services essential. Furthermore, the rising volume of healthcare providers, coupled with the expanding scope of healthcare delivery, leads to an increased need for efficient and accurate credentialing processes. CVOs offer scalability and expertise that healthcare organizations may lack internally, providing a cost-effective solution. Technological advancements, such as cloud-based platforms and AI-powered tools, are significantly streamlining the credentialing process, accelerating turnaround times and reducing manual errors. These technological improvements enhance efficiency and improve accuracy, attracting more healthcare providers to utilize CVO services. Finally, the growing focus on risk management within healthcare organizations is also boosting demand. CVOs offer robust risk mitigation strategies, helping organizations avoid potential legal liabilities and financial penalties associated with non-compliance.

Challenges and Restraints in CVO Credentialing Services

Despite the significant growth potential, the CVO credentialing services market faces certain challenges. Data security and privacy concerns are paramount, given the sensitive nature of provider information handled by CVOs. Maintaining stringent data protection measures and adhering to HIPAA regulations is a critical aspect that necessitates substantial investment in robust cybersecurity infrastructure. Another significant challenge lies in the integration of diverse data sources and systems. Consolidating information from various sources, including state licensing boards, professional organizations, and claims databases, can be complex and time-consuming, requiring sophisticated data management capabilities. Furthermore, maintaining accurate and up-to-date information about provider credentials is crucial. Changes in licensing, certifications, and sanctions require continuous monitoring and updates, posing operational challenges. Finally, competitive pricing pressures and the need to maintain profitability while offering competitive services also impact the market. CVOs must strike a balance between providing high-quality services and managing costs effectively to remain competitive.

Key Region or Country & Segment to Dominate the Market

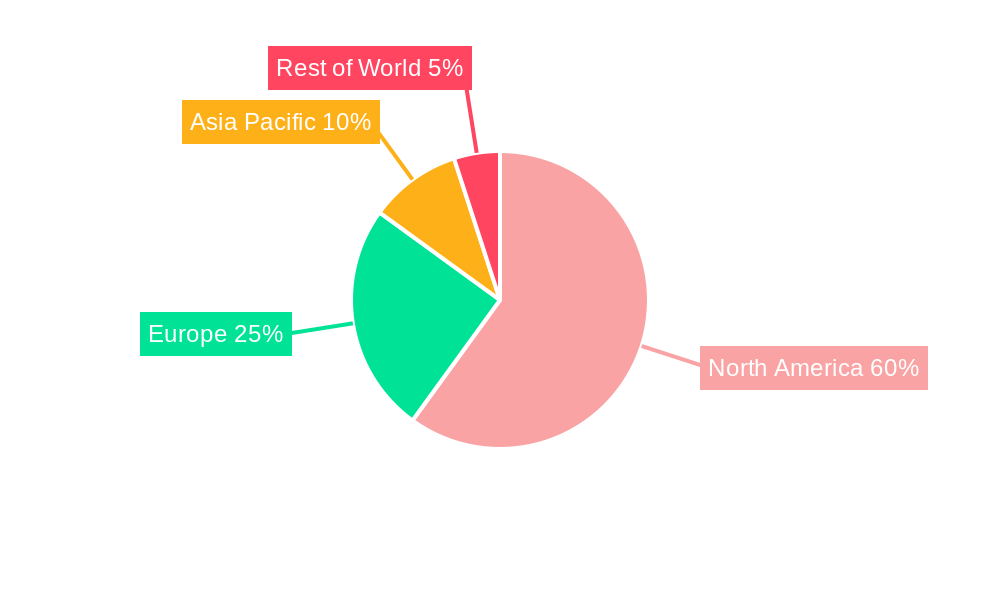

The CVO credentialing services market is geographically diverse, with growth expected across various regions. However, the North American market (primarily the United States) is expected to maintain a dominant position due to its well-established healthcare system, stringent regulatory environment, and a high concentration of healthcare providers. Within specific segments:

Hospitals: This segment holds a significant market share due to the large number of providers requiring credentialing and re-credentialing within large hospital networks. The complex nature of hospital credentialing processes necessitates the expertise and efficiency offered by CVOs.

Initial and Re-credentialing: This segment represents a substantial portion of the market due to the ongoing need for both initial credentialing for new providers and periodic re-credentialing for existing ones. The continuous nature of this requirement drives consistent demand.

Expirables Management: The increasing complexity of managing licenses, certifications, and other credentials with varied expiration dates contributes to this segment's growth. Efficient management of expirations is critical for compliance.

The sheer volume of providers within hospitals, coupled with the continuous cycle of initial and re-credentialing, coupled with the ever-increasing need for proactive expirable management across these larger hospital systems ensures these segments show exponential growth potential within the next decade. Other segments like clinics, DME companies, and home health agencies also contribute significantly, but the scale of hospital operations and the complexities of their credentialing requirements drive the largest market share.

Growth Catalysts in CVO Credentialing Services Industry

The CVO credentialing services industry's growth is fueled by increased regulatory compliance pressures, a surge in healthcare providers, and technological advancements that streamline processes. The demand for efficient credentialing solutions, alongside the rising need for risk mitigation within healthcare organizations, significantly contributes to the industry's expansion. The incorporation of advanced technologies further accelerates the growth trajectory.

Leading Players in the CVO Credentialing Services Market

- VerityStream

- RT Welter

- Advantum Health

- symplr

- Medallion

- Medversant

- Silversheet

- Aperture Health

- The Reference Company

- Hospital Services Corporation

- Paramount

- ProviderTrust

- Orlando Health

Significant Developments in CVO Credentialing Services Sector

- 2021: Increased adoption of cloud-based credentialing platforms by major CVOs.

- 2022: Several CVOs launched AI-powered tools to automate aspects of the credentialing process.

- 2023: Regulatory changes in several states impacted credentialing requirements, prompting CVOs to update their services.

Comprehensive Coverage CVO Credentialing Services Report

This report offers a comprehensive overview of the CVO credentialing services market, covering market size, growth drivers, challenges, and key players. It provides valuable insights into market trends and forecasts, helping stakeholders make informed business decisions. The detailed analysis of key segments and regions offers a granular understanding of the market dynamics. In addition to this the report shows a detailed overview of all companies and their performance within the study period.

CVO Credentialing Services Segmentation

-

1. Application

- 1.1. Clinics

- 1.2. Hospitals

- 1.3. DME Companies

- 1.4. Home Health Agencies

- 1.5. Others

-

2. Type

- 2.1. Initial and Re-credentialing

- 2.2. Expirables Management

- 2.3. Sanctions Monitoring

CVO Credentialing Services Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

CVO Credentialing Services REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Frequently Asked Questions

Table Of Content

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global CVO Credentialing Services Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Clinics

- 5.1.2. Hospitals

- 5.1.3. DME Companies

- 5.1.4. Home Health Agencies

- 5.1.5. Others

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Initial and Re-credentialing

- 5.2.2. Expirables Management

- 5.2.3. Sanctions Monitoring

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America CVO Credentialing Services Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Clinics

- 6.1.2. Hospitals

- 6.1.3. DME Companies

- 6.1.4. Home Health Agencies

- 6.1.5. Others

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Initial and Re-credentialing

- 6.2.2. Expirables Management

- 6.2.3. Sanctions Monitoring

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America CVO Credentialing Services Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Clinics

- 7.1.2. Hospitals

- 7.1.3. DME Companies

- 7.1.4. Home Health Agencies

- 7.1.5. Others

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Initial and Re-credentialing

- 7.2.2. Expirables Management

- 7.2.3. Sanctions Monitoring

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe CVO Credentialing Services Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Clinics

- 8.1.2. Hospitals

- 8.1.3. DME Companies

- 8.1.4. Home Health Agencies

- 8.1.5. Others

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Initial and Re-credentialing

- 8.2.2. Expirables Management

- 8.2.3. Sanctions Monitoring

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa CVO Credentialing Services Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Clinics

- 9.1.2. Hospitals

- 9.1.3. DME Companies

- 9.1.4. Home Health Agencies

- 9.1.5. Others

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Initial and Re-credentialing

- 9.2.2. Expirables Management

- 9.2.3. Sanctions Monitoring

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific CVO Credentialing Services Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Clinics

- 10.1.2. Hospitals

- 10.1.3. DME Companies

- 10.1.4. Home Health Agencies

- 10.1.5. Others

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Initial and Re-credentialing

- 10.2.2. Expirables Management

- 10.2.3. Sanctions Monitoring

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 VerityStream

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 RT Welter

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Advantum Health

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 symplr

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Medallion

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Medversant

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Silversheet

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Aperture Health

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 The Reference Company

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Hospital Services Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Paramount

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 ProviderTrust

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Orlando Health

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.1 VerityStream

List of Figures

- Figure 1: Global CVO Credentialing Services Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America CVO Credentialing Services Revenue (million), by Application 2024 & 2032

- Figure 3: North America CVO Credentialing Services Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America CVO Credentialing Services Revenue (million), by Type 2024 & 2032

- Figure 5: North America CVO Credentialing Services Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America CVO Credentialing Services Revenue (million), by Country 2024 & 2032

- Figure 7: North America CVO Credentialing Services Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America CVO Credentialing Services Revenue (million), by Application 2024 & 2032

- Figure 9: South America CVO Credentialing Services Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America CVO Credentialing Services Revenue (million), by Type 2024 & 2032

- Figure 11: South America CVO Credentialing Services Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America CVO Credentialing Services Revenue (million), by Country 2024 & 2032

- Figure 13: South America CVO Credentialing Services Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe CVO Credentialing Services Revenue (million), by Application 2024 & 2032

- Figure 15: Europe CVO Credentialing Services Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe CVO Credentialing Services Revenue (million), by Type 2024 & 2032

- Figure 17: Europe CVO Credentialing Services Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe CVO Credentialing Services Revenue (million), by Country 2024 & 2032

- Figure 19: Europe CVO Credentialing Services Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa CVO Credentialing Services Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa CVO Credentialing Services Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa CVO Credentialing Services Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa CVO Credentialing Services Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa CVO Credentialing Services Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa CVO Credentialing Services Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific CVO Credentialing Services Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific CVO Credentialing Services Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific CVO Credentialing Services Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific CVO Credentialing Services Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific CVO Credentialing Services Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific CVO Credentialing Services Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global CVO Credentialing Services Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global CVO Credentialing Services Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global CVO Credentialing Services Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global CVO Credentialing Services Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global CVO Credentialing Services Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global CVO Credentialing Services Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global CVO Credentialing Services Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global CVO Credentialing Services Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global CVO Credentialing Services Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global CVO Credentialing Services Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global CVO Credentialing Services Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global CVO Credentialing Services Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global CVO Credentialing Services Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global CVO Credentialing Services Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global CVO Credentialing Services Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global CVO Credentialing Services Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global CVO Credentialing Services Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global CVO Credentialing Services Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global CVO Credentialing Services Revenue million Forecast, by Country 2019 & 2032

- Table 41: China CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific CVO Credentialing Services Revenue (million) Forecast, by Application 2019 & 2032

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

STEP 1 - Identification of Relevant Samples Size from Population Database

STEP 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Top-down and bottom-up approaches are used to validate the global market size and estimate the market size for manufactures, regional segemnts, product and application.

Note* : In applicable scenarios

STEP 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

STEP 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

Additionally after gathering mix and scattered data from wide range of sources, data is triangull- ated and correlated to come up with estimated figures which are further validated through primary mediums, or industry experts, opinion leader.

About Market Research Forecast

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.