Glycol Ethers

Glycol EthersGlycol Ethers Unlocking Growth Potential: Analysis and Forecasts 2025-2033

Glycol Ethers by Type (Propylene oxide-based (P-series), Ethylene oxide-based (E-series)), by Application (Construction, Automotive, Paint & coatings, Cosmetic and personal care, Other), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

Glycol Ethers Unlocking Growth Potential: Analysis and Forecasts 2025-2033

Glycol Ethers Unlocking Growth Potential: Analysis and Forecasts 2025-2033

Key Insights

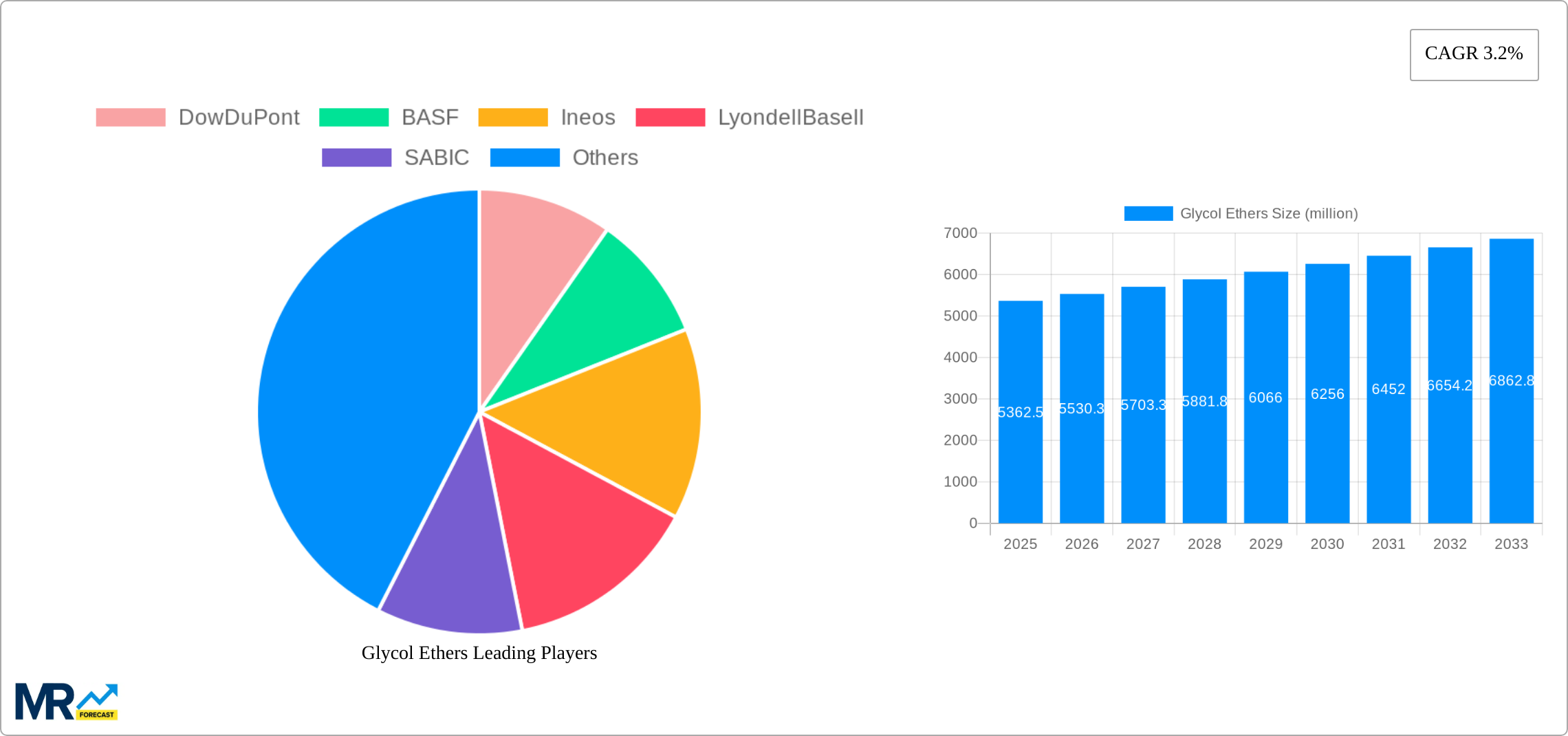

The global glycol ethers market, valued at $5,362.5 million in 2025, is projected to experience steady growth, driven by increasing demand across diverse sectors. The construction industry's reliance on glycol ethers as solvents and additives in paints, coatings, and adhesives significantly fuels market expansion. The automotive industry's use in brake fluids and other components also contributes substantially. Further growth is propelled by the rising popularity of glycol ethers in cosmetic and personal care products due to their solvent and emulsifying properties. The market segmentation, with propylene oxide-based (P-series) and ethylene oxide-based (E-series) glycol ethers holding significant shares, reflects the diverse applications and varying performance characteristics. Geographical distribution shows a strong presence in North America and Europe, driven by established industries and high consumption rates. However, Asia Pacific is poised for significant growth, fueled by rapid industrialization and expanding construction and automotive sectors in countries like China and India. While regulatory constraints on certain applications and the availability of alternative solvents may pose some challenges, the overall outlook for the glycol ethers market remains positive, with a projected Compound Annual Growth Rate (CAGR) of 3.2% from 2025 to 2033. This sustained growth is anticipated to be fueled by ongoing innovation and the development of more sustainable and environmentally friendly formulations within the industry.

Competition in the glycol ethers market is fierce, with major players including DowDuPont, BASF, Ineos, LyondellBasell, SABIC, Formosa Plastics, Reliance, Shell, Sinopec, Huntsman, Eastman Chemical, and others vying for market share through technological advancements, strategic partnerships, and geographical expansion. The market's future trajectory will be shaped by factors such as technological innovations leading to enhanced product performance and sustainability, fluctuating raw material prices, evolving regulatory landscapes, and shifts in consumer preferences towards eco-friendly products. Companies are focusing on developing high-performance glycol ethers with improved properties, such as reduced toxicity and enhanced biodegradability, to meet the growing demand for sustainable solutions. The focus on sustainable practices and stringent environmental regulations will likely influence future market growth and the competitive landscape.

Glycol Ethers Trends

The global glycol ethers market exhibited robust growth throughout the historical period (2019-2024), exceeding several million units in annual sales. This upward trajectory is projected to continue throughout the forecast period (2025-2033), driven by increasing demand across diverse industrial sectors. The estimated market value in 2025 stands at several hundred million units, a testament to its importance in various applications. Key market insights reveal a strong correlation between economic growth in developing nations and the demand for glycol ethers. These versatile chemicals are essential components in numerous products, from paints and coatings to automotive fluids and personal care items. The market is witnessing a shift towards sustainable and environmentally friendly manufacturing processes, spurred by stricter regulations and growing consumer awareness. This is prompting manufacturers to invest in R&D to develop more eco-friendly glycol ether alternatives and production methods. The competitive landscape is characterized by a mix of large multinational corporations and smaller specialty chemical producers, leading to ongoing innovation and price competition. Regional variations in demand are also significant, with certain regions experiencing faster growth due to factors such as burgeoning construction activities and automotive production. The market is expected to be shaped by several external forces, including fluctuations in raw material prices, evolving regulatory landscapes, and technological advancements in production technologies. The balance of these factors will ultimately determine the precise growth trajectory and market share distribution among key players in the coming years. A detailed analysis of these influencing factors across various geographical regions and application segments provides a comprehensive understanding of the market dynamics and future outlook.

Driving Forces: What's Propelling the Glycol Ethers Market?

Several key factors contribute to the strong growth of the glycol ethers market. The expanding construction industry globally is a primary driver, as glycol ethers are crucial components in paints, coatings, and adhesives. The automotive sector's continuous expansion, particularly in developing economies, further fuels demand due to their use in brake fluids, coolants, and other automotive applications. The burgeoning cosmetic and personal care industry, with its focus on innovative formulations, also contributes significantly. Furthermore, the increasing demand for high-performance coatings in various industries, including aerospace and electronics, drives the need for specialized glycol ethers. Technological advancements in the production processes of glycol ethers, leading to improved efficiency and reduced costs, are also pushing market growth. Finally, the diverse range of applications for glycol ethers, combined with their unique properties, like excellent solvency and low toxicity, makes them indispensable in many manufacturing processes. The ongoing research and development efforts focused on improving their performance characteristics and expanding their applications further solidify their position within the chemical market.

Challenges and Restraints in the Glycol Ethers Market

Despite the positive outlook, the glycol ether market faces certain challenges. Fluctuations in the price of raw materials, particularly propylene oxide and ethylene oxide, significantly impact profitability. Stringent environmental regulations and increasing concerns about the potential health effects of certain glycol ethers are leading to increased scrutiny and potential limitations on their use in specific applications. The emergence of alternative solvents and additives that offer comparable performance but with a lower environmental footprint poses a competitive threat. Economic downturns and fluctuations in global demand for end-use products like paints and coatings can also impact glycol ether consumption. Competition from established and emerging players can create pressure on pricing and margins. Finally, the complexities of handling and transporting glycol ethers, particularly those with high toxicity, add to the overall cost and logistical challenges of the industry. These factors represent ongoing hurdles that market players must navigate to maintain sustainable growth.

Key Region or Country & Segment to Dominate the Market

The Asia-Pacific region is expected to dominate the glycol ethers market throughout the forecast period, fueled by rapid industrialization, significant construction activities, and a booming automotive sector. Within this region, China, India, and Southeast Asian nations are key contributors to the growth.

- Asia-Pacific: High growth in construction, automotive, and coatings industries.

- North America: Steady growth driven by established markets and technological advancements.

- Europe: Moderate growth with a focus on sustainable and environmentally friendly alternatives.

Dominant Segments:

- Propylene oxide-based (P-series) glycol ethers: These ethers offer superior performance in several applications, leading to higher demand and market share. Their versatility in terms of solvent properties, and their use in coatings that require high performance and durability, is contributing to their growth. The P-series are often preferred due to their lower toxicity compared to some E-series options and are therefore favored in certain applications (such as those involved in personal care).

- Paint & Coatings Application: This segment continues to be the largest consumer of glycol ethers due to their crucial role in enhancing the properties of paints and coatings, including adhesion, flow, and leveling. The ongoing growth in construction and automotive industries directly impacts the demand in this segment.

The paint and coatings segment is predicted to maintain a substantial share of the market, fueled by the robust growth in the construction and automotive sectors, along with growing demand from other industries. The increasing preference for high-performance coatings that require specialized properties further contributes to the segment's dominance. The P-series glycol ethers are gaining traction due to their superior performance and versatility compared to E-series counterparts in several paint and coating applications.

Growth Catalysts in the Glycol Ethers Industry

The glycol ethers industry is poised for continued growth due to several key factors. Rising demand from various end-use sectors, particularly construction, automotive, and personal care, is a primary catalyst. Technological advancements resulting in more efficient and cost-effective manufacturing processes further fuel expansion. The ongoing research and development efforts toward developing more sustainable and environmentally friendly glycol ethers are crucial for long-term growth, addressing consumer and regulatory concerns.

Leading Players in the Glycol Ethers Market

- DowDuPont

- BASF

- Ineos

- LyondellBasell

- SABIC

- Formosa Plastics

- Reliance

- Shell

- Sinopec

- Huntsman

- Eastman Chemical

Significant Developments in the Glycol Ethers Sector

- 2020: Several major players announced investments in new production facilities to meet the rising global demand.

- 2021: Introduction of several new, more sustainable glycol ether formulations by key manufacturers.

- 2022: Increased focus on life cycle assessments and environmental impact studies of glycol ethers.

- 2023: Several mergers and acquisitions reshaped the competitive landscape of the industry.

Comprehensive Coverage Glycol Ethers Report

This report offers a detailed analysis of the glycol ethers market, providing valuable insights into its growth drivers, challenges, and future outlook. It offers a comprehensive overview of the market trends, leading players, and key segments, providing valuable information for strategic decision-making in this dynamic industry. The detailed regional analysis and segment-specific data allow for a nuanced understanding of market dynamics, enabling businesses to identify lucrative opportunities and mitigate potential risks. The report’s forecast extends to 2033, providing a long-term perspective on the market’s trajectory.

Glycol Ethers Segmentation

-

1. Type

- 1.1. Propylene oxide-based (P-series)

- 1.2. Ethylene oxide-based (E-series)

-

2. Application

- 2.1. Construction

- 2.2. Automotive

- 2.3. Paint & coatings

- 2.4. Cosmetic and personal care

- 2.5. Other

Glycol Ethers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Glycol Ethers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.2% from 2019-2033 |

| Segmentation |

|

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Glycol Ethers Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Propylene oxide-based (P-series)

- 5.1.2. Ethylene oxide-based (E-series)

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Construction

- 5.2.2. Automotive

- 5.2.3. Paint & coatings

- 5.2.4. Cosmetic and personal care

- 5.2.5. Other

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Glycol Ethers Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Propylene oxide-based (P-series)

- 6.1.2. Ethylene oxide-based (E-series)

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Construction

- 6.2.2. Automotive

- 6.2.3. Paint & coatings

- 6.2.4. Cosmetic and personal care

- 6.2.5. Other

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. South America Glycol Ethers Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Propylene oxide-based (P-series)

- 7.1.2. Ethylene oxide-based (E-series)

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Construction

- 7.2.2. Automotive

- 7.2.3. Paint & coatings

- 7.2.4. Cosmetic and personal care

- 7.2.5. Other

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Glycol Ethers Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Propylene oxide-based (P-series)

- 8.1.2. Ethylene oxide-based (E-series)

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Construction

- 8.2.2. Automotive

- 8.2.3. Paint & coatings

- 8.2.4. Cosmetic and personal care

- 8.2.5. Other

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East & Africa Glycol Ethers Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Propylene oxide-based (P-series)

- 9.1.2. Ethylene oxide-based (E-series)

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Construction

- 9.2.2. Automotive

- 9.2.3. Paint & coatings

- 9.2.4. Cosmetic and personal care

- 9.2.5. Other

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific Glycol Ethers Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Propylene oxide-based (P-series)

- 10.1.2. Ethylene oxide-based (E-series)

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Construction

- 10.2.2. Automotive

- 10.2.3. Paint & coatings

- 10.2.4. Cosmetic and personal care

- 10.2.5. Other

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 DowDuPont

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 BASF

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Ineos

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 LyondellBasell

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SABIC

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Formosa Plastics

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Reliance

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Shell

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Sinopec

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Huntsman

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Eastman Chemical

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 DowDuPont

- Figure 1: Global Glycol Ethers Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: Global Glycol Ethers Volume Breakdown (K, %) by Region 2024 & 2032

- Figure 3: North America Glycol Ethers Revenue (million), by Type 2024 & 2032

- Figure 4: North America Glycol Ethers Volume (K), by Type 2024 & 2032

- Figure 5: North America Glycol Ethers Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Glycol Ethers Volume Share (%), by Type 2024 & 2032

- Figure 7: North America Glycol Ethers Revenue (million), by Application 2024 & 2032

- Figure 8: North America Glycol Ethers Volume (K), by Application 2024 & 2032

- Figure 9: North America Glycol Ethers Revenue Share (%), by Application 2024 & 2032

- Figure 10: North America Glycol Ethers Volume Share (%), by Application 2024 & 2032

- Figure 11: North America Glycol Ethers Revenue (million), by Country 2024 & 2032

- Figure 12: North America Glycol Ethers Volume (K), by Country 2024 & 2032

- Figure 13: North America Glycol Ethers Revenue Share (%), by Country 2024 & 2032

- Figure 14: North America Glycol Ethers Volume Share (%), by Country 2024 & 2032

- Figure 15: South America Glycol Ethers Revenue (million), by Type 2024 & 2032

- Figure 16: South America Glycol Ethers Volume (K), by Type 2024 & 2032

- Figure 17: South America Glycol Ethers Revenue Share (%), by Type 2024 & 2032

- Figure 18: South America Glycol Ethers Volume Share (%), by Type 2024 & 2032

- Figure 19: South America Glycol Ethers Revenue (million), by Application 2024 & 2032

- Figure 20: South America Glycol Ethers Volume (K), by Application 2024 & 2032

- Figure 21: South America Glycol Ethers Revenue Share (%), by Application 2024 & 2032

- Figure 22: South America Glycol Ethers Volume Share (%), by Application 2024 & 2032

- Figure 23: South America Glycol Ethers Revenue (million), by Country 2024 & 2032

- Figure 24: South America Glycol Ethers Volume (K), by Country 2024 & 2032

- Figure 25: South America Glycol Ethers Revenue Share (%), by Country 2024 & 2032

- Figure 26: South America Glycol Ethers Volume Share (%), by Country 2024 & 2032

- Figure 27: Europe Glycol Ethers Revenue (million), by Type 2024 & 2032

- Figure 28: Europe Glycol Ethers Volume (K), by Type 2024 & 2032

- Figure 29: Europe Glycol Ethers Revenue Share (%), by Type 2024 & 2032

- Figure 30: Europe Glycol Ethers Volume Share (%), by Type 2024 & 2032

- Figure 31: Europe Glycol Ethers Revenue (million), by Application 2024 & 2032

- Figure 32: Europe Glycol Ethers Volume (K), by Application 2024 & 2032

- Figure 33: Europe Glycol Ethers Revenue Share (%), by Application 2024 & 2032

- Figure 34: Europe Glycol Ethers Volume Share (%), by Application 2024 & 2032

- Figure 35: Europe Glycol Ethers Revenue (million), by Country 2024 & 2032

- Figure 36: Europe Glycol Ethers Volume (K), by Country 2024 & 2032

- Figure 37: Europe Glycol Ethers Revenue Share (%), by Country 2024 & 2032

- Figure 38: Europe Glycol Ethers Volume Share (%), by Country 2024 & 2032

- Figure 39: Middle East & Africa Glycol Ethers Revenue (million), by Type 2024 & 2032

- Figure 40: Middle East & Africa Glycol Ethers Volume (K), by Type 2024 & 2032

- Figure 41: Middle East & Africa Glycol Ethers Revenue Share (%), by Type 2024 & 2032

- Figure 42: Middle East & Africa Glycol Ethers Volume Share (%), by Type 2024 & 2032

- Figure 43: Middle East & Africa Glycol Ethers Revenue (million), by Application 2024 & 2032

- Figure 44: Middle East & Africa Glycol Ethers Volume (K), by Application 2024 & 2032

- Figure 45: Middle East & Africa Glycol Ethers Revenue Share (%), by Application 2024 & 2032

- Figure 46: Middle East & Africa Glycol Ethers Volume Share (%), by Application 2024 & 2032

- Figure 47: Middle East & Africa Glycol Ethers Revenue (million), by Country 2024 & 2032

- Figure 48: Middle East & Africa Glycol Ethers Volume (K), by Country 2024 & 2032

- Figure 49: Middle East & Africa Glycol Ethers Revenue Share (%), by Country 2024 & 2032

- Figure 50: Middle East & Africa Glycol Ethers Volume Share (%), by Country 2024 & 2032

- Figure 51: Asia Pacific Glycol Ethers Revenue (million), by Type 2024 & 2032

- Figure 52: Asia Pacific Glycol Ethers Volume (K), by Type 2024 & 2032

- Figure 53: Asia Pacific Glycol Ethers Revenue Share (%), by Type 2024 & 2032

- Figure 54: Asia Pacific Glycol Ethers Volume Share (%), by Type 2024 & 2032

- Figure 55: Asia Pacific Glycol Ethers Revenue (million), by Application 2024 & 2032

- Figure 56: Asia Pacific Glycol Ethers Volume (K), by Application 2024 & 2032

- Figure 57: Asia Pacific Glycol Ethers Revenue Share (%), by Application 2024 & 2032

- Figure 58: Asia Pacific Glycol Ethers Volume Share (%), by Application 2024 & 2032

- Figure 59: Asia Pacific Glycol Ethers Revenue (million), by Country 2024 & 2032

- Figure 60: Asia Pacific Glycol Ethers Volume (K), by Country 2024 & 2032

- Figure 61: Asia Pacific Glycol Ethers Revenue Share (%), by Country 2024 & 2032

- Figure 62: Asia Pacific Glycol Ethers Volume Share (%), by Country 2024 & 2032

- Table 1: Global Glycol Ethers Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Glycol Ethers Volume K Forecast, by Region 2019 & 2032

- Table 3: Global Glycol Ethers Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Glycol Ethers Volume K Forecast, by Type 2019 & 2032

- Table 5: Global Glycol Ethers Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Glycol Ethers Volume K Forecast, by Application 2019 & 2032

- Table 7: Global Glycol Ethers Revenue million Forecast, by Region 2019 & 2032

- Table 8: Global Glycol Ethers Volume K Forecast, by Region 2019 & 2032

- Table 9: Global Glycol Ethers Revenue million Forecast, by Type 2019 & 2032

- Table 10: Global Glycol Ethers Volume K Forecast, by Type 2019 & 2032

- Table 11: Global Glycol Ethers Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Glycol Ethers Volume K Forecast, by Application 2019 & 2032

- Table 13: Global Glycol Ethers Revenue million Forecast, by Country 2019 & 2032

- Table 14: Global Glycol Ethers Volume K Forecast, by Country 2019 & 2032

- Table 15: United States Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: United States Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 17: Canada Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 18: Canada Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 19: Mexico Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 20: Mexico Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 21: Global Glycol Ethers Revenue million Forecast, by Type 2019 & 2032

- Table 22: Global Glycol Ethers Volume K Forecast, by Type 2019 & 2032

- Table 23: Global Glycol Ethers Revenue million Forecast, by Application 2019 & 2032

- Table 24: Global Glycol Ethers Volume K Forecast, by Application 2019 & 2032

- Table 25: Global Glycol Ethers Revenue million Forecast, by Country 2019 & 2032

- Table 26: Global Glycol Ethers Volume K Forecast, by Country 2019 & 2032

- Table 27: Brazil Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Brazil Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 29: Argentina Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 30: Argentina Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 31: Rest of South America Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 32: Rest of South America Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 33: Global Glycol Ethers Revenue million Forecast, by Type 2019 & 2032

- Table 34: Global Glycol Ethers Volume K Forecast, by Type 2019 & 2032

- Table 35: Global Glycol Ethers Revenue million Forecast, by Application 2019 & 2032

- Table 36: Global Glycol Ethers Volume K Forecast, by Application 2019 & 2032

- Table 37: Global Glycol Ethers Revenue million Forecast, by Country 2019 & 2032

- Table 38: Global Glycol Ethers Volume K Forecast, by Country 2019 & 2032

- Table 39: United Kingdom Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 40: United Kingdom Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 41: Germany Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: Germany Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 43: France Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: France Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 45: Italy Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Italy Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 47: Spain Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 48: Spain Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 49: Russia Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 50: Russia Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 51: Benelux Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 52: Benelux Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 53: Nordics Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 54: Nordics Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 55: Rest of Europe Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 56: Rest of Europe Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 57: Global Glycol Ethers Revenue million Forecast, by Type 2019 & 2032

- Table 58: Global Glycol Ethers Volume K Forecast, by Type 2019 & 2032

- Table 59: Global Glycol Ethers Revenue million Forecast, by Application 2019 & 2032

- Table 60: Global Glycol Ethers Volume K Forecast, by Application 2019 & 2032

- Table 61: Global Glycol Ethers Revenue million Forecast, by Country 2019 & 2032

- Table 62: Global Glycol Ethers Volume K Forecast, by Country 2019 & 2032

- Table 63: Turkey Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 64: Turkey Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 65: Israel Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 66: Israel Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 67: GCC Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 68: GCC Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 69: North Africa Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 70: North Africa Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 71: South Africa Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 72: South Africa Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 73: Rest of Middle East & Africa Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 74: Rest of Middle East & Africa Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 75: Global Glycol Ethers Revenue million Forecast, by Type 2019 & 2032

- Table 76: Global Glycol Ethers Volume K Forecast, by Type 2019 & 2032

- Table 77: Global Glycol Ethers Revenue million Forecast, by Application 2019 & 2032

- Table 78: Global Glycol Ethers Volume K Forecast, by Application 2019 & 2032

- Table 79: Global Glycol Ethers Revenue million Forecast, by Country 2019 & 2032

- Table 80: Global Glycol Ethers Volume K Forecast, by Country 2019 & 2032

- Table 81: China Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 82: China Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 83: India Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 84: India Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 85: Japan Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 86: Japan Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 87: South Korea Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 88: South Korea Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 89: ASEAN Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 90: ASEAN Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 91: Oceania Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 92: Oceania Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

- Table 93: Rest of Asia Pacific Glycol Ethers Revenue (million) Forecast, by Application 2019 & 2032

- Table 94: Rest of Asia Pacific Glycol Ethers Volume (K) Forecast, by Application 2019 & 2032

STEP 1 - Identification of Relevant Samples Size from Population Database

STEP 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note* : In applicable scenarios

STEP 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

STEP 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

Frequently Asked Questions

Related Reports

About Market Research Forecast

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.