Industrial Metal Scrap Recycling Service

Industrial Metal Scrap Recycling ServiceIndustrial Metal Scrap Recycling Service 2025-2033 Analysis: Trends, Competitor Dynamics, and Growth Opportunities

Industrial Metal Scrap Recycling Service by Type (Iron, Copper, Aluminum, Others), by Application (Building and Construction, Automotive, Electrical and Electronics, Industrial Machinery, Others), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

Industrial Metal Scrap Recycling Service 2025-2033 Analysis: Trends, Competitor Dynamics, and Growth Opportunities

Key Insights

The global industrial metal scrap recycling market is experiencing robust growth, driven by increasing urbanization, industrialization, and stringent environmental regulations promoting sustainable resource management. The market's value in 2025 is estimated at $150 billion, exhibiting a Compound Annual Growth Rate (CAGR) of 5% from 2025 to 2033. This growth is fueled by rising demand for recycled metals across various sectors, including building and construction, automotive, and electrical and electronics manufacturing. The construction boom in developing economies and the shift towards electric vehicles are major contributors. Iron, copper, and aluminum scrap constitute the largest segments, driven by their widespread applications. However, the market faces challenges such as fluctuating metal prices, technological limitations in processing certain scrap types, and inconsistent waste management infrastructure in some regions.

Despite these restraints, several trends are shaping the market's future. Technological advancements in scrap processing and sorting, enabling better recovery rates and higher-quality recycled materials, are crucial. The rise of circular economy initiatives and government policies supporting recycling are creating a favorable regulatory environment. The increasing adoption of automation and data analytics in scrap management improves efficiency and reduces operating costs. Key players are focusing on strategic partnerships, acquisitions, and technological innovation to maintain their competitive edge. Geographical expansion, particularly into emerging markets with high scrap generation potential, is also a key strategy. The market segmentation by metal type and application reflects diverse demand patterns, and regional variations depend on economic development levels and regulatory frameworks. The forecast period from 2025 to 2033 indicates substantial growth potential, with North America, Europe, and Asia-Pacific remaining leading markets.

Industrial Metal Scrap Recycling Service Trends

The global industrial metal scrap recycling service market is experiencing robust growth, projected to reach multi-billion dollar valuations by 2033. Driven by increasing environmental consciousness, stringent regulations on waste disposal, and the rising demand for recycled metals in various industries, the market shows significant promise. The historical period (2019-2024) witnessed a steady increase in recycling activities, particularly in developed nations with established infrastructure and regulations. The base year (2025) marks a crucial point, reflecting the consolidated impact of post-pandemic economic recovery and increased focus on sustainability initiatives. The forecast period (2025-2033) anticipates a continued upward trajectory, fueled by technological advancements in sorting and processing techniques, leading to improved efficiency and higher-quality recycled materials. This growth is not uniform across all metal types; while ferrous metals (iron and steel) currently dominate the market due to their high volume and established recycling networks, the demand for non-ferrous metals like copper and aluminum is rapidly escalating, driven by the burgeoning electronics and automotive sectors. The market dynamics are further shaped by fluctuating raw material prices, which influence the economic viability of scrap recycling. Geographical variations also exist, with regions possessing advanced infrastructure and supportive government policies witnessing faster growth compared to others. The market is characterized by a mix of large multinational corporations and smaller regional players, fostering both intense competition and opportunities for strategic partnerships and acquisitions. Overall, the industrial metal scrap recycling service market is poised for considerable expansion, reflecting a global shift towards a more circular economy.

Driving Forces: What's Propelling the Industrial Metal Scrap Recycling Service

Several key factors are driving the expansion of the industrial metal scrap recycling service market. Firstly, the escalating global demand for metals across diverse sectors, from construction and automotive to electronics and industrial machinery, is creating a substantial need for cost-effective and sustainable metal sourcing. Recycled metals offer a significantly more affordable alternative compared to virgin materials, providing a crucial economic incentive for recycling. Secondly, the growing awareness of environmental concerns and the urgent need to reduce carbon emissions are placing immense pressure on industries to adopt sustainable practices. Metal recycling plays a vital role in minimizing landfill waste, conserving natural resources, and reducing the environmental impact associated with metal extraction and processing. Government regulations and policies worldwide are increasingly promoting metal recycling through incentives, tax breaks, and stricter regulations on waste disposal, further bolstering market growth. Technological advancements in metal sorting, processing, and purification techniques are also enhancing the efficiency and quality of recycled metals, making them more appealing to end-users. Finally, the increasing adoption of circular economy models and the growing focus on resource efficiency are creating a favorable environment for the expansion of the industrial metal scrap recycling service market, underpinning its long-term sustainability.

Challenges and Restraints in Industrial Metal Scrap Recycling Service

Despite the considerable growth potential, the industrial metal scrap recycling service market faces several challenges. Fluctuating metal prices pose a significant risk, impacting the profitability of recycling operations. Variations in metal prices can make recycling economically unviable at times, particularly for less valuable metals. The heterogeneous nature of scrap metal necessitates sophisticated sorting and processing technologies, representing a substantial capital investment for recycling companies. Furthermore, the global distribution of scrap metal poses logistical challenges, particularly in terms of collection, transportation, and storage. The lack of standardized quality control and certification across different scrap processing facilities can hinder the acceptance of recycled metals by end-users who prioritize consistency and reliability. Moreover, contamination of scrap metal with hazardous materials can pose environmental and health risks, requiring careful handling and disposal procedures. In some regions, a lack of adequate infrastructure, including collection centers and processing facilities, can limit the effectiveness of recycling programs. Finally, competition from alternative materials and the need for continuous technological upgrades to remain competitive add further complexity to this market.

Key Region or Country & Segment to Dominate the Market

Iron Segment Dominance: The iron and steel segment holds a significant share of the industrial metal scrap recycling market. Its high volume and established recycling infrastructure contribute to its leading position. The construction, automotive, and industrial machinery sectors heavily rely on iron and steel, driving demand for recycled materials. Recycling iron and steel significantly reduces reliance on virgin materials, lowering production costs and environmental impact.

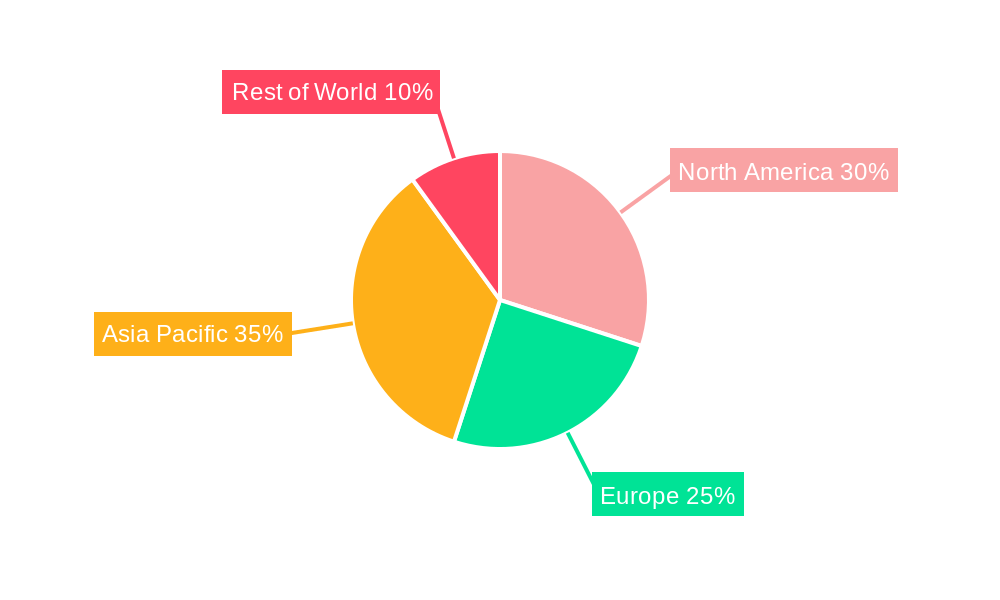

North America and Europe as Key Regions: North America and Europe, particularly countries like the US, Germany, and the UK, are expected to dominate the market due to their established recycling infrastructure, robust regulatory frameworks promoting sustainable practices, and high demand for recycled metals across various sectors. The presence of large multinational recycling companies, combined with a strong awareness of environmental responsibility, fosters a favorable environment for growth in these regions.

- North America: High per capita metal consumption and robust recycling infrastructure provide a fertile ground.

- Europe: Stringent environmental regulations and a strong push towards circular economy initiatives are driving the market.

- Asia-Pacific (Emerging Market): Rapid industrialization and urbanization in countries like China and India are creating significant demand, but infrastructure development remains a key factor.

Building and Construction as a Major Application: The building and construction sector is a major consumer of recycled metals, especially iron and steel. Demolition projects generate large quantities of scrap metal, providing a significant feedstock for recycling. The use of recycled metals in construction contributes to cost savings and reduces the environmental impact of new construction projects. The growing construction activity globally, especially in developing economies, further fuels the demand for recycled metals within this sector.

Growth Potential in Other Segments: While iron dominates currently, there's substantial growth potential in the copper and aluminum segments. The rise of electric vehicles and electronics manufacturing fuels the demand for recycled copper and aluminum, driving innovation and investment in these specific recycling streams.

Growth Catalysts in Industrial Metal Scrap Recycling Service Industry

The industrial metal scrap recycling service industry's growth is catalyzed by several factors: increasing environmental regulations mandating higher recycling rates, a surge in demand for recycled materials driven by cost savings and sustainability concerns, and advancements in recycling technologies that improve efficiency and the quality of recovered metals. Government incentives and policies promoting sustainable practices further bolster this growth. The transition to a circular economy model and increased awareness of responsible resource management among businesses and consumers also contribute to the industry's upward trajectory.

Leading Players in the Industrial Metal Scrap Recycling Service

- Sims Limited

- The David J. Joseph Company

- OmniSource, LLC

- Stena Metall Group

- ATC Metals GmbH

- Aadi Group

- MTC Business Pvt. Ltd.

- Ferrous Processing & Trading Company

- Commercial Metals Company

- ASM Recycling Inc.

Significant Developments in Industrial Metal Scrap Recycling Service Sector

- 2021: Sims Limited announces a major investment in a new state-of-the-art metal recycling facility in Europe.

- 2022: Several major players announce partnerships to improve the collection and processing of e-waste, focusing on precious metals recovery.

- 2023: New regulations in several countries introduce stricter standards for metal recycling and waste management, boosting the market.

Comprehensive Coverage Industrial Metal Scrap Recycling Service Report

This report provides a comprehensive analysis of the industrial metal scrap recycling service market, offering insights into market trends, growth drivers, challenges, and key players. It offers detailed segment analyses (by metal type and application) and regional breakdowns, allowing for a thorough understanding of this dynamic sector's current state and future prospects. The report utilizes robust data and projections, covering the historical period (2019-2024), base year (2025), and forecast period (2025-2033), providing a valuable resource for businesses, investors, and policymakers involved in or interested in this crucial industry.

Industrial Metal Scrap Recycling Service Segmentation

-

1. Type

- 1.1. Iron

- 1.2. Copper

- 1.3. Aluminum

- 1.4. Others

-

2. Application

- 2.1. Building and Construction

- 2.2. Automotive

- 2.3. Electrical and Electronics

- 2.4. Industrial Machinery

- 2.5. Others

Industrial Metal Scrap Recycling Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Industrial Metal Scrap Recycling Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Frequently Asked Questions

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Industrial Metal Scrap Recycling Service Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Iron

- 5.1.2. Copper

- 5.1.3. Aluminum

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Building and Construction

- 5.2.2. Automotive

- 5.2.3. Electrical and Electronics

- 5.2.4. Industrial Machinery

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Industrial Metal Scrap Recycling Service Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Iron

- 6.1.2. Copper

- 6.1.3. Aluminum

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Building and Construction

- 6.2.2. Automotive

- 6.2.3. Electrical and Electronics

- 6.2.4. Industrial Machinery

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. South America Industrial Metal Scrap Recycling Service Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Iron

- 7.1.2. Copper

- 7.1.3. Aluminum

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Building and Construction

- 7.2.2. Automotive

- 7.2.3. Electrical and Electronics

- 7.2.4. Industrial Machinery

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Industrial Metal Scrap Recycling Service Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Iron

- 8.1.2. Copper

- 8.1.3. Aluminum

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Building and Construction

- 8.2.2. Automotive

- 8.2.3. Electrical and Electronics

- 8.2.4. Industrial Machinery

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East & Africa Industrial Metal Scrap Recycling Service Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Iron

- 9.1.2. Copper

- 9.1.3. Aluminum

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Building and Construction

- 9.2.2. Automotive

- 9.2.3. Electrical and Electronics

- 9.2.4. Industrial Machinery

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific Industrial Metal Scrap Recycling Service Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Iron

- 10.1.2. Copper

- 10.1.3. Aluminum

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Building and Construction

- 10.2.2. Automotive

- 10.2.3. Electrical and Electronics

- 10.2.4. Industrial Machinery

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 Sims Limited

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 The David J. Joseph Company

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 OmniSource LLC

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Stena Metall Group

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 ATC Metals GmbH

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Aadi Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 MTC Business Pvt. Ltd.

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Ferrous Processing & Trading Company

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Commercial Metals Company

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 ASM Recycling Inc.

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Sims Limited

- Figure 1: Global Industrial Metal Scrap Recycling Service Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Industrial Metal Scrap Recycling Service Revenue (million), by Type 2024 & 2032

- Figure 3: North America Industrial Metal Scrap Recycling Service Revenue Share (%), by Type 2024 & 2032

- Figure 4: North America Industrial Metal Scrap Recycling Service Revenue (million), by Application 2024 & 2032

- Figure 5: North America Industrial Metal Scrap Recycling Service Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Industrial Metal Scrap Recycling Service Revenue (million), by Country 2024 & 2032

- Figure 7: North America Industrial Metal Scrap Recycling Service Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Industrial Metal Scrap Recycling Service Revenue (million), by Type 2024 & 2032

- Figure 9: South America Industrial Metal Scrap Recycling Service Revenue Share (%), by Type 2024 & 2032

- Figure 10: South America Industrial Metal Scrap Recycling Service Revenue (million), by Application 2024 & 2032

- Figure 11: South America Industrial Metal Scrap Recycling Service Revenue Share (%), by Application 2024 & 2032

- Figure 12: South America Industrial Metal Scrap Recycling Service Revenue (million), by Country 2024 & 2032

- Figure 13: South America Industrial Metal Scrap Recycling Service Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Industrial Metal Scrap Recycling Service Revenue (million), by Type 2024 & 2032

- Figure 15: Europe Industrial Metal Scrap Recycling Service Revenue Share (%), by Type 2024 & 2032

- Figure 16: Europe Industrial Metal Scrap Recycling Service Revenue (million), by Application 2024 & 2032

- Figure 17: Europe Industrial Metal Scrap Recycling Service Revenue Share (%), by Application 2024 & 2032

- Figure 18: Europe Industrial Metal Scrap Recycling Service Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Industrial Metal Scrap Recycling Service Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Industrial Metal Scrap Recycling Service Revenue (million), by Type 2024 & 2032

- Figure 21: Middle East & Africa Industrial Metal Scrap Recycling Service Revenue Share (%), by Type 2024 & 2032

- Figure 22: Middle East & Africa Industrial Metal Scrap Recycling Service Revenue (million), by Application 2024 & 2032

- Figure 23: Middle East & Africa Industrial Metal Scrap Recycling Service Revenue Share (%), by Application 2024 & 2032

- Figure 24: Middle East & Africa Industrial Metal Scrap Recycling Service Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Industrial Metal Scrap Recycling Service Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Industrial Metal Scrap Recycling Service Revenue (million), by Type 2024 & 2032

- Figure 27: Asia Pacific Industrial Metal Scrap Recycling Service Revenue Share (%), by Type 2024 & 2032

- Figure 28: Asia Pacific Industrial Metal Scrap Recycling Service Revenue (million), by Application 2024 & 2032

- Figure 29: Asia Pacific Industrial Metal Scrap Recycling Service Revenue Share (%), by Application 2024 & 2032

- Figure 30: Asia Pacific Industrial Metal Scrap Recycling Service Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Industrial Metal Scrap Recycling Service Revenue Share (%), by Country 2024 & 2032

- Table 1: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Type 2019 & 2032

- Table 3: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Application 2019 & 2032

- Table 7: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Application 2019 & 2032

- Table 13: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Type 2019 & 2032

- Table 18: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Application 2019 & 2032

- Table 19: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Type 2019 & 2032

- Table 30: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Application 2019 & 2032

- Table 31: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Type 2019 & 2032

- Table 39: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Application 2019 & 2032

- Table 40: Global Industrial Metal Scrap Recycling Service Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Industrial Metal Scrap Recycling Service Revenue (million) Forecast, by Application 2019 & 2032

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

STEP 1 - Identification of Relevant Samples Size from Population Database

STEP 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note* : In applicable scenarios

STEP 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

STEP 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

Related Reports

About Market Research Forecast

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.