Infectious Disease In-vitro Diagnostic

Infectious Disease In-vitro DiagnosticInfectious Disease In-vitro Diagnostic Report Probes the 58 million Size, Share, Growth Report and Future Analysis by 2033

Infectious Disease In-vitro Diagnostic by Type (Immunoassay, Molecular Diagnostics, Microbiology, Others), by Application (COVID-19, MRSA, Clostridium Difficile, Respiratory Virus, TB and Drug-resistant TB, Chlamydia, Gonorrhea, HPV, HIV, Others(Gastro-intestinal Panel Testing, Hepatitis C, Hepatitis B, etc)), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

Infectious Disease In-vitro Diagnostic Report Probes the 58 million Size, Share, Growth Report and Future Analysis by 2033

Infectious Disease In-vitro Diagnostic Report Probes the 58 million Size, Share, Growth Report and Future Analysis by 2033

Key Insights

The global infectious disease in-vitro diagnostic (IVD) market, valued at $58 million in 2025, is projected to experience steady growth, driven by several key factors. The increasing prevalence of infectious diseases, particularly drug-resistant strains like MRSA and tuberculosis, necessitates advanced diagnostic tools for timely and accurate detection. This demand fuels the market expansion, especially within molecular diagnostics and immunoassay segments, which offer high sensitivity and specificity. Furthermore, the rising geriatric population, increasing healthcare expenditure, and advancements in diagnostic technologies, such as rapid diagnostic tests (RDTs) and point-of-care testing (POCT), contribute to market growth. Government initiatives promoting disease surveillance and control programs, coupled with rising investments in research and development of new diagnostic assays, also positively impact market dynamics. Geographic expansion, particularly in emerging economies with growing healthcare infrastructure, presents lucrative opportunities. However, factors like high costs associated with advanced technologies, stringent regulatory approvals, and the potential for diagnostic errors pose challenges to market growth.

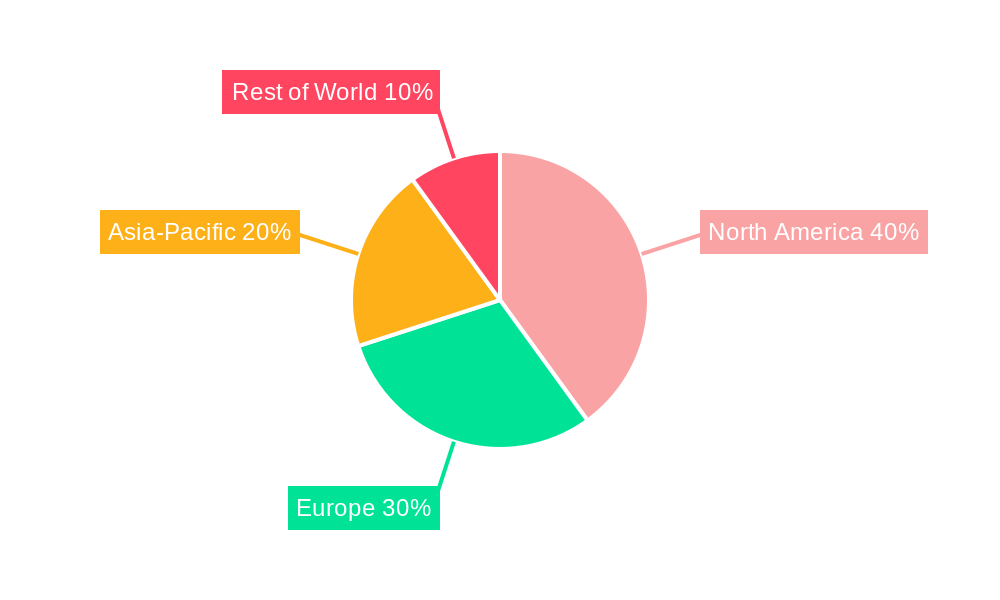

Despite these challenges, the market is segmented by various infectious diseases, including COVID-19 (which, while experiencing a decline in immediate impact, continues to drive demand for related testing), respiratory viruses, and sexually transmitted infections (STIs) like Chlamydia, Gonorrhea, and HPV. The market also incorporates segments for various technologies such as immunoassays, molecular diagnostics, and microbiology. The competitive landscape comprises major players like BD, BioMérieux, Abbott, and Roche, each contributing to technological advancements and market share. Considering a CAGR of 3.7%, the market size is estimated to expand significantly over the forecast period (2025-2033), with specific growth rates varying among regions based on healthcare infrastructure, disease prevalence, and economic factors. North America and Europe are expected to retain significant market share due to established healthcare systems and robust diagnostic infrastructure. However, Asia-Pacific is likely to witness faster growth due to expanding healthcare investment and increasing infectious disease prevalence.

Infectious Disease In-vitro Diagnostic Trends

The infectious disease in-vitro diagnostic (IVD) market is experiencing robust growth, driven by several converging factors. The global market size is projected to reach multi-billion-dollar valuations by 2033, expanding significantly from its valuation in 2024. This expansion is fueled by increasing prevalence of infectious diseases, both globally and within specific regions, coupled with advancements in diagnostic technologies. The demand for rapid, accurate, and cost-effective diagnostic tools is continually rising, leading to innovation in areas like molecular diagnostics and point-of-care testing. The COVID-19 pandemic acted as a significant catalyst, accelerating the adoption of advanced IVD technologies and highlighting the critical role of rapid diagnostics in pandemic response. This surge in demand, however, is not limited to pandemic-related diseases. The market also witnesses consistent growth in diagnostics for other prevalent infectious diseases like tuberculosis, HIV, and sexually transmitted infections. The increasing geriatric population, also, poses a challenge given their increased susceptibility to infections. Furthermore, the rise in antibiotic-resistant bacteria is spurring the development and adoption of novel diagnostic solutions, further fueling market expansion. The market is witnessing a shift towards decentralized testing, with an increased focus on point-of-care diagnostics to enable faster diagnosis and treatment initiation closer to the patient. This trend is further driven by the need for improved healthcare access in remote and underserved areas. The market is characterized by a competitive landscape with numerous established players and emerging companies vying for market share through innovation and strategic acquisitions.

Driving Forces: What's Propelling the Infectious Disease In-vitro Diagnostic Market?

Several factors are propelling the growth of the infectious disease IVD market. The rising incidence of infectious diseases worldwide, including the emergence of new and drug-resistant strains, is a primary driver. This necessitates the development and adoption of sophisticated diagnostic tools capable of identifying these pathogens quickly and accurately. Technological advancements in areas such as molecular diagnostics (PCR, next-generation sequencing), immunoassays, and rapid diagnostic tests (RDTs) are significantly impacting market growth. These innovations offer improved sensitivity, specificity, and speed compared to traditional methods. Furthermore, the increasing prevalence of chronic diseases, weakening the immune system and making individuals more susceptible to infections, contributes significantly to market growth. Government initiatives and funding aimed at improving public health infrastructure and disease surveillance programs are also bolstering market expansion. The growing demand for personalized medicine, along with a greater focus on point-of-care testing, enhances accessibility and affordability. This facilitates early diagnosis and prompt treatment, resulting in improved patient outcomes and reduced healthcare costs in the long run. Finally, the rising awareness about the importance of infectious disease prevention and control among the general population contributes to a heightened demand for reliable and accessible diagnostic tests.

Challenges and Restraints in Infectious Disease In-vitro Diagnostic Market

Despite the significant growth potential, the infectious disease IVD market faces several challenges. High development and manufacturing costs associated with innovative diagnostic technologies can limit market accessibility, especially in low- and middle-income countries. Regulatory hurdles and stringent approval processes for new diagnostic tests pose a barrier to market entry and can delay the launch of promising technologies. The reimbursement policies for IVD tests vary significantly across different healthcare systems, which impacts market access and profitability. Furthermore, the potential for inaccuracies in test results, especially with less sophisticated technologies, poses concerns regarding treatment efficacy and patient safety. Ensuring the quality and reliability of diagnostic tests is crucial to building trust and maintaining market confidence. The complex logistics associated with the transportation and storage of certain diagnostic reagents and samples can affect testing efficiency and results, particularly in areas with limited infrastructure. Finally, the need for skilled personnel to operate and interpret the results from complex diagnostic technologies remains a significant hurdle, especially in areas with limited healthcare worker availability.

Key Region or Country & Segment to Dominate the Market

The molecular diagnostics segment is projected to dominate the infectious disease IVD market due to its high sensitivity and specificity in detecting various pathogens. This segment's growth is further fueled by the increasing adoption of PCR-based tests and next-generation sequencing technologies. The COVID-19 application segment experienced a significant surge during the pandemic and is expected to sustain considerable growth, given the potential for future outbreaks. However, growth in applications beyond COVID-19 are also projected to be significant. The market for diagnostics for respiratory viruses, including influenza and RSV, is also predicted to experience substantial growth driven by increasing prevalence and demand for rapid diagnostic testing.

- North America and Europe are currently the leading markets, driven by advanced healthcare infrastructure, high healthcare expenditure, and strong regulatory frameworks. However, rapidly developing economies in Asia-Pacific are showing significant potential, fueled by rising infectious disease burden and increasing healthcare investments.

- The tuberculosis (TB) and drug-resistant TB application segment is also expected to witness considerable growth due to the global burden of TB and the rising incidence of drug-resistant strains. The demand for rapid, sensitive, and specific diagnostic tests for TB detection and drug susceptibility testing is increasing rapidly, driving the growth of this segment. Within this segment, molecular diagnostics techniques are gaining considerable traction, offering faster turnaround times compared to traditional culture-based methods and enabling effective treatment strategies.

Growth in the immunoassay segment is expected to be driven by factors such as its ease of use and relatively low cost compared to molecular diagnostics. It remains a crucial segment for the detection of various infectious diseases. However, molecular diagnostics is expected to gradually take a larger market share due to its superior performance characteristics.

The market is expected to witness significant growth in the point-of-care testing segment, driven by the rising need for rapid and accessible diagnostics in various settings, including primary care clinics, hospitals, and remote areas.

Growth Catalysts in Infectious Disease In-vitro Diagnostic Industry

The infectious disease IVD market is experiencing a wave of innovation, with several factors driving its expansion. Technological advancements, particularly in molecular diagnostics and point-of-care testing, are playing a pivotal role. Increased funding for research and development from both public and private sectors fuels this innovation pipeline, fostering the creation of more sensitive, specific, and rapid diagnostic tests. Simultaneously, heightened public awareness regarding infectious diseases, coupled with government initiatives promoting disease surveillance and prevention, fosters market growth by driving demand for diagnostic services. These factors, along with the ongoing need for effective pandemic preparedness and response, contribute significantly to the market’s expanding potential.

Leading Players in the Infectious Disease In-vitro Diagnostic Market

- BD

- BioMérieux SA

- Abbott

- Quidel Corporation

- OraSure Technologies, Inc.

- Hologic, Inc. (Gen Probe)

- Danaher

- QIAGEN

- Roche

- Siemens Healthineers AG

- Bio-Rad Laboratories, Inc.

Significant Developments in Infectious Disease In-vitro Diagnostic Sector

- 2020: Several companies rapidly developed and launched COVID-19 diagnostic tests.

- 2021: Increased focus on point-of-care testing for various infectious diseases.

- 2022: Several mergers and acquisitions within the IVD sector occurred to expand market reach and product portfolio.

- 2023: Advances in AI and machine learning are being integrated into diagnostic platforms to improve accuracy and speed.

- 2024: Focus on developing diagnostics for antimicrobial-resistant pathogens gains momentum.

Comprehensive Coverage Infectious Disease In-vitro Diagnostic Report

This report provides a detailed analysis of the infectious disease IVD market, covering market trends, drivers, restraints, key players, and significant developments. The report offers a comprehensive understanding of the market dynamics, enabling stakeholders to make informed decisions. It presents forecasts for market growth and segmentation, providing valuable insights into future market trends and opportunities. This detailed overview will help inform strategic planning and investments in this rapidly evolving sector.

Infectious Disease In-vitro Diagnostic Segmentation

-

1. Type

- 1.1. Immunoassay

- 1.2. Molecular Diagnostics

- 1.3. Microbiology

- 1.4. Others

-

2. Application

- 2.1. COVID-19

- 2.2. MRSA

- 2.3. Clostridium Difficile

- 2.4. Respiratory Virus

- 2.5. TB and Drug-resistant TB

- 2.6. Chlamydia

- 2.7. Gonorrhea

- 2.8. HPV

- 2.9. HIV

- 2.10. Others(Gastro-intestinal Panel Testing, Hepatitis C, Hepatitis B, etc)

Infectious Disease In-vitro Diagnostic Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Infectious Disease In-vitro Diagnostic REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.7% from 2019-2033 |

| Segmentation |

|

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Infectious Disease In-vitro Diagnostic Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Immunoassay

- 5.1.2. Molecular Diagnostics

- 5.1.3. Microbiology

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. COVID-19

- 5.2.2. MRSA

- 5.2.3. Clostridium Difficile

- 5.2.4. Respiratory Virus

- 5.2.5. TB and Drug-resistant TB

- 5.2.6. Chlamydia

- 5.2.7. Gonorrhea

- 5.2.8. HPV

- 5.2.9. HIV

- 5.2.10. Others(Gastro-intestinal Panel Testing, Hepatitis C, Hepatitis B, etc)

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. North America Infectious Disease In-vitro Diagnostic Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Immunoassay

- 6.1.2. Molecular Diagnostics

- 6.1.3. Microbiology

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. COVID-19

- 6.2.2. MRSA

- 6.2.3. Clostridium Difficile

- 6.2.4. Respiratory Virus

- 6.2.5. TB and Drug-resistant TB

- 6.2.6. Chlamydia

- 6.2.7. Gonorrhea

- 6.2.8. HPV

- 6.2.9. HIV

- 6.2.10. Others(Gastro-intestinal Panel Testing, Hepatitis C, Hepatitis B, etc)

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. South America Infectious Disease In-vitro Diagnostic Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Immunoassay

- 7.1.2. Molecular Diagnostics

- 7.1.3. Microbiology

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. COVID-19

- 7.2.2. MRSA

- 7.2.3. Clostridium Difficile

- 7.2.4. Respiratory Virus

- 7.2.5. TB and Drug-resistant TB

- 7.2.6. Chlamydia

- 7.2.7. Gonorrhea

- 7.2.8. HPV

- 7.2.9. HIV

- 7.2.10. Others(Gastro-intestinal Panel Testing, Hepatitis C, Hepatitis B, etc)

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Infectious Disease In-vitro Diagnostic Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Immunoassay

- 8.1.2. Molecular Diagnostics

- 8.1.3. Microbiology

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. COVID-19

- 8.2.2. MRSA

- 8.2.3. Clostridium Difficile

- 8.2.4. Respiratory Virus

- 8.2.5. TB and Drug-resistant TB

- 8.2.6. Chlamydia

- 8.2.7. Gonorrhea

- 8.2.8. HPV

- 8.2.9. HIV

- 8.2.10. Others(Gastro-intestinal Panel Testing, Hepatitis C, Hepatitis B, etc)

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East & Africa Infectious Disease In-vitro Diagnostic Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Immunoassay

- 9.1.2. Molecular Diagnostics

- 9.1.3. Microbiology

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. COVID-19

- 9.2.2. MRSA

- 9.2.3. Clostridium Difficile

- 9.2.4. Respiratory Virus

- 9.2.5. TB and Drug-resistant TB

- 9.2.6. Chlamydia

- 9.2.7. Gonorrhea

- 9.2.8. HPV

- 9.2.9. HIV

- 9.2.10. Others(Gastro-intestinal Panel Testing, Hepatitis C, Hepatitis B, etc)

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Asia Pacific Infectious Disease In-vitro Diagnostic Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Immunoassay

- 10.1.2. Molecular Diagnostics

- 10.1.3. Microbiology

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. COVID-19

- 10.2.2. MRSA

- 10.2.3. Clostridium Difficile

- 10.2.4. Respiratory Virus

- 10.2.5. TB and Drug-resistant TB

- 10.2.6. Chlamydia

- 10.2.7. Gonorrhea

- 10.2.8. HPV

- 10.2.9. HIV

- 10.2.10. Others(Gastro-intestinal Panel Testing, Hepatitis C, Hepatitis B, etc)

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 BD

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 BioMérieux SA

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Abbott

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Quidel Corporation

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 OraSure Technologies Inc.

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Hologic Inc. (Gen Probe)

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Danaher

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 QIAGEN

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Roche

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Siemens Healthineers AG

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Bio-Rad Laboratories Inc.

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 BD

- Figure 1: Global Infectious Disease In-vitro Diagnostic Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Infectious Disease In-vitro Diagnostic Revenue (million), by Type 2024 & 2032

- Figure 3: North America Infectious Disease In-vitro Diagnostic Revenue Share (%), by Type 2024 & 2032

- Figure 4: North America Infectious Disease In-vitro Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 5: North America Infectious Disease In-vitro Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 6: North America Infectious Disease In-vitro Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 7: North America Infectious Disease In-vitro Diagnostic Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Infectious Disease In-vitro Diagnostic Revenue (million), by Type 2024 & 2032

- Figure 9: South America Infectious Disease In-vitro Diagnostic Revenue Share (%), by Type 2024 & 2032

- Figure 10: South America Infectious Disease In-vitro Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 11: South America Infectious Disease In-vitro Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 12: South America Infectious Disease In-vitro Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 13: South America Infectious Disease In-vitro Diagnostic Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Infectious Disease In-vitro Diagnostic Revenue (million), by Type 2024 & 2032

- Figure 15: Europe Infectious Disease In-vitro Diagnostic Revenue Share (%), by Type 2024 & 2032

- Figure 16: Europe Infectious Disease In-vitro Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 17: Europe Infectious Disease In-vitro Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 18: Europe Infectious Disease In-vitro Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Infectious Disease In-vitro Diagnostic Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Infectious Disease In-vitro Diagnostic Revenue (million), by Type 2024 & 2032

- Figure 21: Middle East & Africa Infectious Disease In-vitro Diagnostic Revenue Share (%), by Type 2024 & 2032

- Figure 22: Middle East & Africa Infectious Disease In-vitro Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 23: Middle East & Africa Infectious Disease In-vitro Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 24: Middle East & Africa Infectious Disease In-vitro Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Infectious Disease In-vitro Diagnostic Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Infectious Disease In-vitro Diagnostic Revenue (million), by Type 2024 & 2032

- Figure 27: Asia Pacific Infectious Disease In-vitro Diagnostic Revenue Share (%), by Type 2024 & 2032

- Figure 28: Asia Pacific Infectious Disease In-vitro Diagnostic Revenue (million), by Application 2024 & 2032

- Figure 29: Asia Pacific Infectious Disease In-vitro Diagnostic Revenue Share (%), by Application 2024 & 2032

- Figure 30: Asia Pacific Infectious Disease In-vitro Diagnostic Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Infectious Disease In-vitro Diagnostic Revenue Share (%), by Country 2024 & 2032

- Table 1: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Type 2019 & 2032

- Table 3: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 4: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Type 2019 & 2032

- Table 6: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 7: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Type 2019 & 2032

- Table 12: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 13: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Type 2019 & 2032

- Table 18: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 19: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Type 2019 & 2032

- Table 30: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 31: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Type 2019 & 2032

- Table 39: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Application 2019 & 2032

- Table 40: Global Infectious Disease In-vitro Diagnostic Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Infectious Disease In-vitro Diagnostic Revenue (million) Forecast, by Application 2019 & 2032

STEP 1 - Identification of Relevant Samples Size from Population Database

STEP 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note* : In applicable scenarios

STEP 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

STEP 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

Frequently Asked Questions

Related Reports

About Market Research Forecast

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.