Pulp Transport Service

Pulp Transport ServicePulp Transport Service Unlocking Growth Potential: Analysis and Forecasts 2025-2033

Pulp Transport Service by Application (Dry Pulp, Wet Pulp), by Type (Pulp Ship:≤ 40000 Tons, Pulp Ship: More than 40000 Tons), by North America (United States, Canada, Mexico), by South America (Brazil, Argentina, Rest of South America), by Europe (United Kingdom, Germany, France, Italy, Spain, Russia, Benelux, Nordics, Rest of Europe), by Middle East & Africa (Turkey, Israel, GCC, North Africa, South Africa, Rest of Middle East & Africa), by Asia Pacific (China, India, Japan, South Korea, ASEAN, Oceania, Rest of Asia Pacific) Forecast 2025-2033

Pulp Transport Service Unlocking Growth Potential: Analysis and Forecasts 2025-2033

Key Insights

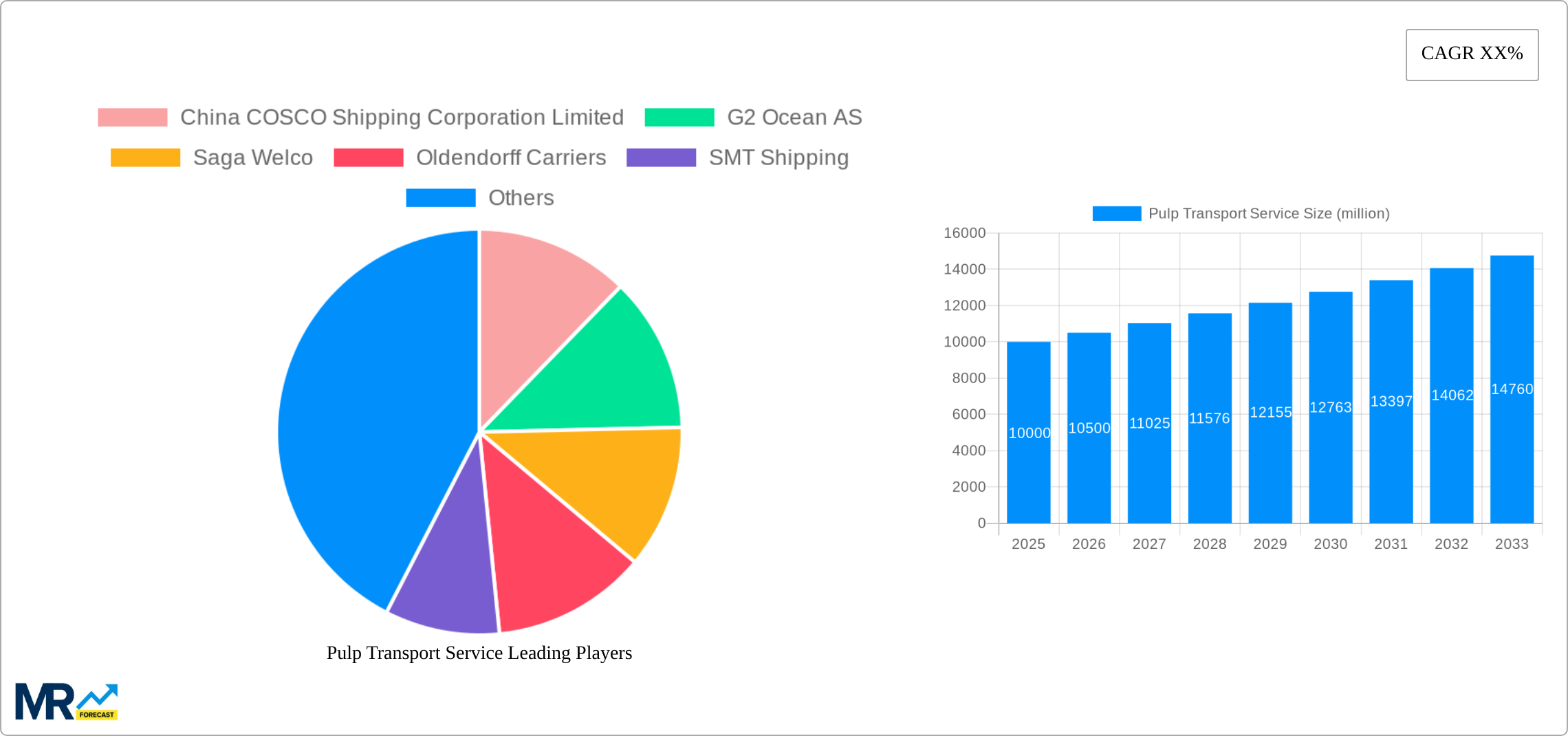

The global pulp transport service market is experiencing robust growth, driven by the increasing demand for paper and pulp products across diverse sectors. The market, estimated at $10 billion in 2025, is projected to exhibit a Compound Annual Growth Rate (CAGR) of 5% from 2025 to 2033, reaching approximately $14 billion by 2033. This growth is fueled by several key factors, including the expansion of the paper and packaging industries, particularly in developing economies like China and India. Furthermore, the rising adoption of sustainable forestry practices and the increasing demand for eco-friendly packaging solutions are positively influencing market expansion. The segmentation by application (dry pulp vs. wet pulp) and vessel size (<40,000 tons vs. >40,000 tons) reflects differing transportation needs and associated cost structures. Dry pulp transportation, for example, often necessitates specialized handling and potentially higher costs, while larger vessels offer economies of scale for wet pulp transportation.

Key players in the market, including China COSCO Shipping, G2 Ocean, and others, are actively investing in modernizing their fleets and enhancing logistics capabilities to meet the rising demand. However, market growth may be tempered by factors such as fluctuating fuel prices, geopolitical instability, and potential disruptions to global supply chains. Regional variations in market share are expected, with Asia-Pacific, particularly China, anticipated to maintain a significant lead due to its substantial pulp production and consumption. North America and Europe will also contribute significantly, driven by robust demand within their respective regions. Overall, the market presents substantial opportunities for growth and innovation, particularly for companies capable of adapting to evolving transportation needs and maintaining efficient logistics operations within a dynamic global landscape.

Pulp Transport Service Trends

The global pulp transport service market, valued at approximately $XX million in 2024, is projected to reach $YY million by 2033, exhibiting a CAGR of Z% during the forecast period (2025-2033). The historical period (2019-2024) witnessed moderate growth, largely driven by the increasing demand for pulp in paper and packaging industries. However, the forecast period anticipates a more significant surge, fueled by several factors detailed below. The base year for this analysis is 2025, and the study period spans 2019-2033. Key market insights reveal a shift towards larger pulp ships (more than 40,000 tons) to achieve economies of scale and reduce transportation costs. This trend is particularly noticeable in long-haul routes connecting major pulp-producing regions like Scandinavia and South America with key consumption centers in Asia and North America. Furthermore, the market is experiencing a growing demand for specialized services catering to specific pulp types, such as dry and wet pulp, necessitating tailored shipping solutions and increased logistical coordination. The competitive landscape is dynamic, with established players like China COSCO Shipping Corporation Limited and Oldendorff Carriers vying for market share alongside emerging specialized carriers. The increasing focus on sustainability and environmental regulations is also influencing market dynamics, prompting a greater emphasis on efficient and environmentally friendly transportation practices. The growth is further influenced by fluctuating pulp prices, global economic conditions, and geopolitical factors impacting trade routes and shipping costs.

Driving Forces: What's Propelling the Pulp Transport Service

Several factors are contributing to the growth of the pulp transport service market. Firstly, the rising global demand for paper and paperboard products, particularly in developing economies with expanding populations and increasing urbanization, is a key driver. This increased demand translates directly into a higher need for pulp transportation. Secondly, the growth of the packaging industry, especially for e-commerce and fast-moving consumer goods, is significantly boosting pulp demand. Packaging often utilizes pulp-based materials, further fueling the need for efficient pulp transport services. Thirdly, technological advancements in pulp processing and shipping are leading to greater efficiency and cost optimization. Larger, more specialized vessels are being utilized, minimizing transportation costs per unit of pulp. Lastly, the ongoing consolidation within the shipping industry is leading to stronger market players with improved service offerings and greater global reach. These factors collectively contribute to a positive outlook for the pulp transport market, projecting substantial growth in the coming years.

Challenges and Restraints in Pulp Transport Service

Despite the positive growth outlook, the pulp transport service industry faces several challenges. Fluctuations in pulp prices and global commodity markets create uncertainty in pricing and profitability for shipping companies. Geopolitical instability and disruptions to global trade routes, such as port congestion and international conflicts, can significantly impact transport times and costs. Stringent environmental regulations regarding emissions and waste management are increasing operational costs for shipping companies, pushing them towards more sustainable but potentially more expensive solutions. Furthermore, the intensity of competition within the shipping industry, with many companies vying for market share, can lead to price wars and reduced profit margins. The unpredictable nature of weather patterns and potential natural disasters can disrupt shipping schedules and increase transportation risks. Finally, the skilled labor shortage in the maritime industry can affect the availability and cost of qualified personnel to operate and maintain shipping vessels.

Key Region or Country & Segment to Dominate the Market

The Asia-Pacific region is expected to dominate the pulp transport service market, driven by the burgeoning paper and packaging industries in countries like China, India, and Southeast Asia. This region's high pulp consumption coupled with its expanding manufacturing base creates a high demand for efficient and reliable pulp transportation.

Segment Dominance: The segment of "Pulp Ship: More than 40,000 Tons" is projected to hold a significant market share. This is due to economies of scale; larger ships drastically reduce the cost per unit of pulp transported, particularly on long-haul routes. The increasing efficiency and cost-effectiveness of using larger vessels are making them the preferred choice for many major pulp producers and importers. This segment benefits from ongoing investments in infrastructure and logistics to support the handling and berthing of these larger ships. Furthermore, the optimization of shipping routes and logistical planning for these larger vessels is another key driver. While the smaller pulp ship segment (≤40,000 Tons) will continue to exist, its market share is expected to decline relative to the larger vessel segment over the forecast period.

Dry Pulp: Dry pulp represents a substantial portion of the market due to its widespread use in paper production and other applications. The transportation of dry pulp presents a slightly lower logistical challenge compared to wet pulp and its lower sensitivity to waterborne risks.

Geographic Distribution: North America and Europe also play significant roles, but the Asia-Pacific region's growth trajectory is unmatched, making it the most influential market. The strong presence of established pulp and paper companies in Europe means this region will maintain a strong position, though likely to grow at a slower rate than Asia-Pacific. North America will similarly maintain its role driven by robust domestic demand and imports.

Growth Catalysts in Pulp Transport Service Industry

The pulp transport service industry is experiencing robust growth fueled by increasing global demand for pulp, driven largely by expanding paper and packaging sectors, particularly in developing economies. Furthermore, improvements in logistics and shipping technology, including the use of larger, more efficient vessels, are contributing to cost reductions and increased efficiency. The ongoing consolidation within the industry is creating larger, more powerful players with enhanced capabilities for handling global pulp transport.

Leading Players in the Pulp Transport Service

- China COSCO Shipping Corporation Limited

- G2 Ocean AS

- Saga Welco

- Oldendorff Carriers

- SMT Shipping

- MUR Shipping BV

- Lauritzen Bulkers A/S

- Toko Kaiun Kaisha Ltd

- Pan Ocean Co Ltd

- Taylor Maritime HK Ltd

- GMB Maritime Liner Services

Significant Developments in Pulp Transport Service Sector

- 2020: Several major pulp transport companies invested heavily in digitalization to improve tracking and logistics.

- 2021: New environmental regulations impacting emissions came into effect, prompting investment in greener shipping technologies.

- 2022: A significant number of mergers and acquisitions occurred within the industry, reshaping the competitive landscape.

- 2023: Several new large-capacity pulp carriers were launched, driving cost efficiency.

Comprehensive Coverage Pulp Transport Service Report

This report provides a detailed analysis of the pulp transport service market, offering comprehensive insights into market trends, drivers, challenges, and key players. It includes detailed forecasts for the forecast period, segmented by application (dry and wet pulp), vessel type (≤ 40,000 tons and >40,000 tons), and geographic regions. The report serves as a valuable resource for businesses operating in the pulp and paper industry, shipping companies, and investors seeking to understand this dynamic market. It offers actionable insights for strategic decision-making and competitive advantage.

Pulp Transport Service Segmentation

-

1. Application

- 1.1. Dry Pulp

- 1.2. Wet Pulp

-

2. Type

- 2.1. Pulp Ship:≤ 40000 Tons

- 2.2. Pulp Ship: More than 40000 Tons

Pulp Transport Service Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Pulp Transport Service REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

Frequently Asked Questions

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Pulp Transport Service Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Dry Pulp

- 5.1.2. Wet Pulp

- 5.2. Market Analysis, Insights and Forecast - by Type

- 5.2.1. Pulp Ship:≤ 40000 Tons

- 5.2.2. Pulp Ship: More than 40000 Tons

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Pulp Transport Service Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Dry Pulp

- 6.1.2. Wet Pulp

- 6.2. Market Analysis, Insights and Forecast - by Type

- 6.2.1. Pulp Ship:≤ 40000 Tons

- 6.2.2. Pulp Ship: More than 40000 Tons

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Pulp Transport Service Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Dry Pulp

- 7.1.2. Wet Pulp

- 7.2. Market Analysis, Insights and Forecast - by Type

- 7.2.1. Pulp Ship:≤ 40000 Tons

- 7.2.2. Pulp Ship: More than 40000 Tons

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Pulp Transport Service Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Dry Pulp

- 8.1.2. Wet Pulp

- 8.2. Market Analysis, Insights and Forecast - by Type

- 8.2.1. Pulp Ship:≤ 40000 Tons

- 8.2.2. Pulp Ship: More than 40000 Tons

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Pulp Transport Service Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Dry Pulp

- 9.1.2. Wet Pulp

- 9.2. Market Analysis, Insights and Forecast - by Type

- 9.2.1. Pulp Ship:≤ 40000 Tons

- 9.2.2. Pulp Ship: More than 40000 Tons

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Pulp Transport Service Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Dry Pulp

- 10.1.2. Wet Pulp

- 10.2. Market Analysis, Insights and Forecast - by Type

- 10.2.1. Pulp Ship:≤ 40000 Tons

- 10.2.2. Pulp Ship: More than 40000 Tons

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2024

- 11.2. Company Profiles

- 11.2.1 China COSCO Shipping Corporation Limited

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 G2 Ocean AS

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Saga Welco

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Oldendorff Carriers

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 SMT Shipping

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 MUR Shipping BV

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Lauritzen Bulkers A/S

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Toko Kaiun Kaisha Ltd

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Pan Ocean Co Ltd

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Taylor Maritime HK Ltd

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 GMB Maritime Liner Services

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.1 China COSCO Shipping Corporation Limited

- Figure 1: Global Pulp Transport Service Revenue Breakdown (million, %) by Region 2024 & 2032

- Figure 2: North America Pulp Transport Service Revenue (million), by Application 2024 & 2032

- Figure 3: North America Pulp Transport Service Revenue Share (%), by Application 2024 & 2032

- Figure 4: North America Pulp Transport Service Revenue (million), by Type 2024 & 2032

- Figure 5: North America Pulp Transport Service Revenue Share (%), by Type 2024 & 2032

- Figure 6: North America Pulp Transport Service Revenue (million), by Country 2024 & 2032

- Figure 7: North America Pulp Transport Service Revenue Share (%), by Country 2024 & 2032

- Figure 8: South America Pulp Transport Service Revenue (million), by Application 2024 & 2032

- Figure 9: South America Pulp Transport Service Revenue Share (%), by Application 2024 & 2032

- Figure 10: South America Pulp Transport Service Revenue (million), by Type 2024 & 2032

- Figure 11: South America Pulp Transport Service Revenue Share (%), by Type 2024 & 2032

- Figure 12: South America Pulp Transport Service Revenue (million), by Country 2024 & 2032

- Figure 13: South America Pulp Transport Service Revenue Share (%), by Country 2024 & 2032

- Figure 14: Europe Pulp Transport Service Revenue (million), by Application 2024 & 2032

- Figure 15: Europe Pulp Transport Service Revenue Share (%), by Application 2024 & 2032

- Figure 16: Europe Pulp Transport Service Revenue (million), by Type 2024 & 2032

- Figure 17: Europe Pulp Transport Service Revenue Share (%), by Type 2024 & 2032

- Figure 18: Europe Pulp Transport Service Revenue (million), by Country 2024 & 2032

- Figure 19: Europe Pulp Transport Service Revenue Share (%), by Country 2024 & 2032

- Figure 20: Middle East & Africa Pulp Transport Service Revenue (million), by Application 2024 & 2032

- Figure 21: Middle East & Africa Pulp Transport Service Revenue Share (%), by Application 2024 & 2032

- Figure 22: Middle East & Africa Pulp Transport Service Revenue (million), by Type 2024 & 2032

- Figure 23: Middle East & Africa Pulp Transport Service Revenue Share (%), by Type 2024 & 2032

- Figure 24: Middle East & Africa Pulp Transport Service Revenue (million), by Country 2024 & 2032

- Figure 25: Middle East & Africa Pulp Transport Service Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Pulp Transport Service Revenue (million), by Application 2024 & 2032

- Figure 27: Asia Pacific Pulp Transport Service Revenue Share (%), by Application 2024 & 2032

- Figure 28: Asia Pacific Pulp Transport Service Revenue (million), by Type 2024 & 2032

- Figure 29: Asia Pacific Pulp Transport Service Revenue Share (%), by Type 2024 & 2032

- Figure 30: Asia Pacific Pulp Transport Service Revenue (million), by Country 2024 & 2032

- Figure 31: Asia Pacific Pulp Transport Service Revenue Share (%), by Country 2024 & 2032

- Table 1: Global Pulp Transport Service Revenue million Forecast, by Region 2019 & 2032

- Table 2: Global Pulp Transport Service Revenue million Forecast, by Application 2019 & 2032

- Table 3: Global Pulp Transport Service Revenue million Forecast, by Type 2019 & 2032

- Table 4: Global Pulp Transport Service Revenue million Forecast, by Region 2019 & 2032

- Table 5: Global Pulp Transport Service Revenue million Forecast, by Application 2019 & 2032

- Table 6: Global Pulp Transport Service Revenue million Forecast, by Type 2019 & 2032

- Table 7: Global Pulp Transport Service Revenue million Forecast, by Country 2019 & 2032

- Table 8: United States Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 9: Canada Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 11: Global Pulp Transport Service Revenue million Forecast, by Application 2019 & 2032

- Table 12: Global Pulp Transport Service Revenue million Forecast, by Type 2019 & 2032

- Table 13: Global Pulp Transport Service Revenue million Forecast, by Country 2019 & 2032

- Table 14: Brazil Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 15: Argentina Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 16: Rest of South America Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 17: Global Pulp Transport Service Revenue million Forecast, by Application 2019 & 2032

- Table 18: Global Pulp Transport Service Revenue million Forecast, by Type 2019 & 2032

- Table 19: Global Pulp Transport Service Revenue million Forecast, by Country 2019 & 2032

- Table 20: United Kingdom Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 21: Germany Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 22: France Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 23: Italy Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 24: Spain Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 25: Russia Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 26: Benelux Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 27: Nordics Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 28: Rest of Europe Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 29: Global Pulp Transport Service Revenue million Forecast, by Application 2019 & 2032

- Table 30: Global Pulp Transport Service Revenue million Forecast, by Type 2019 & 2032

- Table 31: Global Pulp Transport Service Revenue million Forecast, by Country 2019 & 2032

- Table 32: Turkey Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 33: Israel Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 34: GCC Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 35: North Africa Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 36: South Africa Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 37: Rest of Middle East & Africa Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 38: Global Pulp Transport Service Revenue million Forecast, by Application 2019 & 2032

- Table 39: Global Pulp Transport Service Revenue million Forecast, by Type 2019 & 2032

- Table 40: Global Pulp Transport Service Revenue million Forecast, by Country 2019 & 2032

- Table 41: China Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 42: India Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 43: Japan Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 44: South Korea Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 45: ASEAN Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 46: Oceania Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

- Table 47: Rest of Asia Pacific Pulp Transport Service Revenue (million) Forecast, by Application 2019 & 2032

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of XX% from 2019-2033 |

| Segmentation |

|

STEP 1 - Identification of Relevant Samples Size from Population Database

STEP 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note* : In applicable scenarios

STEP 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

STEP 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence

Related Reports

About Market Research Forecast

MR Forecast provides premium market intelligence on deep technologies that can cause a high level of disruption in the market within the next few years. When it comes to doing market viability analyses for technologies at very early phases of development, MR Forecast is second to none. What sets us apart is our set of market estimates based on secondary research data, which in turn gets validated through primary research by key companies in the target market and other stakeholders. It only covers technologies pertaining to Healthcare, IT, big data analysis, block chain technology, Artificial Intelligence (AI), Machine Learning (ML), Internet of Things (IoT), Energy & Power, Automobile, Agriculture, Electronics, Chemical & Materials, Machinery & Equipment's, Consumer Goods, and many others at MR Forecast. Market: The market section introduces the industry to readers, including an overview, business dynamics, competitive benchmarking, and firms' profiles. This enables readers to make decisions on market entry, expansion, and exit in certain nations, regions, or worldwide. Application: We give painstaking attention to the study of every product and technology, along with its use case and user categories, under our research solutions. From here on, the process delivers accurate market estimates and forecasts apart from the best and most meaningful insights.

Products generically come under this phrase and may imply any number of goods, components, materials, technology, or any combination thereof. Any business that wants to push an innovative agenda needs data on product definitions, pricing analysis, benchmarking and roadmaps on technology, demand analysis, and patents. Our research papers contain all that and much more in a depth that makes them incredibly actionable. Products broadly encompass a wide range of goods, components, materials, technologies, or any combination thereof. For businesses aiming to advance an innovative agenda, access to comprehensive data on product definitions, pricing analysis, benchmarking, technological roadmaps, demand analysis, and patents is essential. Our research papers provide in-depth insights into these areas and more, equipping organizations with actionable information that can drive strategic decision-making and enhance competitive positioning in the market.